I’ve heard this so much it has gotten to the point that is has become “conventional wisdom”. Of course long time readers know that instantly causes our antennas here to go up and dig a little deeper.

First let me say what follows is not an absolute. Economics involves people’s reactions to various stimuli, we cannot say “for certain” what will happen but we can gleam generalities from past behavior. That is the reason for this post.

The basic thesis seems to be that higher 30yr mortgage rates will kill a housing recovery and thus the economic recovery in general. Sounds good….but is it true? The data is less than convincing:

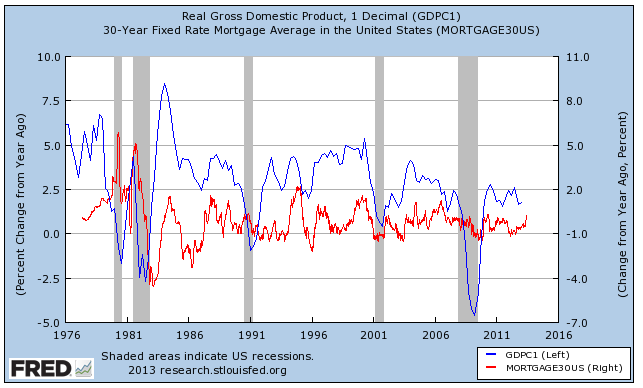

Here is a chart showing the change in real GDP vs the change in the 30yr mortgage. Also, while I have included the dates, we should discount comparisons to the ’78-’81 time frame as the oil crisis, stagflation and Volker’s ratcheting up interest rates skew the period as none of those economic conditions apply now.

What you see is that rising GDP and rising 30yr rates seem to go together and seem to do so for several years at a time. That means that far from damaging housing and the economy immediately, 30yr rates seem to be pulled higher by them. In fact, given the time frame above, it seems as though the business cycle and the periodic inescapable recessions it brings (to varying degrees) has much more to do with the economy than mortgage rates. As the chart shows rates can rise for several years without having any impact on GDP. As general demand in the economy rises, so do rates, when demand falls as we enter recession, rates then follow. If rates directed activity to the degree some suggest, this would not happen.

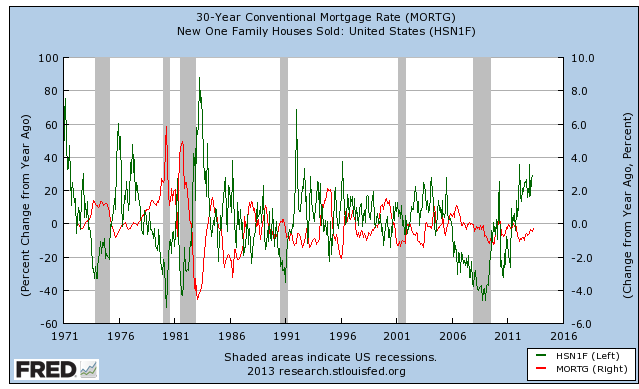

Here are new home sales and 30yr rates (% change YOY)

Like the GDP chart the change in interest rates lags economic activity in both direction and in fact single family sales are volatile even when rates remain steady. Both housing and GDP convincingly turn south or north well before interest rates do. That tells me that interest rates get jerked around in response economic activity rather than the other way around. To be sure at the extremes, interest rates will affect economic activity, but to suggest interest 30yr. rates going from 3.75% to 4% is “bad” for both housing and the economy is simply not backed up by the data.

What is more likely is that as the economy gains strength (particularly housing/auto) rates follow.

How can this be?

Credit. At the low end of the credit rate scale, it is available to only the lowest risk borrowers. Banks cannot get enough spread to expand credit down the line. Sub-prime credit is not a bad thing, if the bank can be properly compensated across the risk spectrum for it. It wasn’t subprime credit per se that caused the last housing collapse, it was the fact that millions of homeowners (both prime and subprime) were allowed to purchase housing without equity (no money down) and mortgages that reset making paying for that home impossible if prices stopped rising. That made walking away easy and in many cases the only option. The borrowers themselves we not that terrible, it was the instruments they were allowed to use to purchase that were.

What policy makers and bankers missed then was because of these new instruments, if prices only stagnated, it meant millions of homeowners were then going to be forced sellers virtually all at once when their AltA (interest only) loans reset no matter what their credit score. Forced selling there, in addition to normal recessionary forced selling (due to job losses) caused a cascade. Equity enables stability.

That has been rectified….anyone who has tried to either refi or buy a home in the last three years understands this.

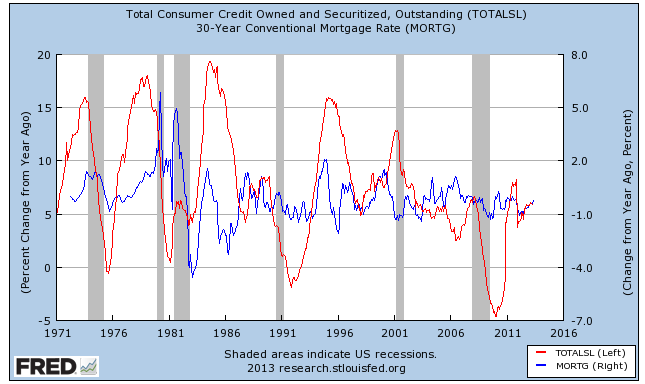

For those who may doubt the “higher rates mean more lending” line of thinking take a look at this chart. Notice Consumer Credit picks up as the 30yr rises YOY and falls as it falls (YOY % change).

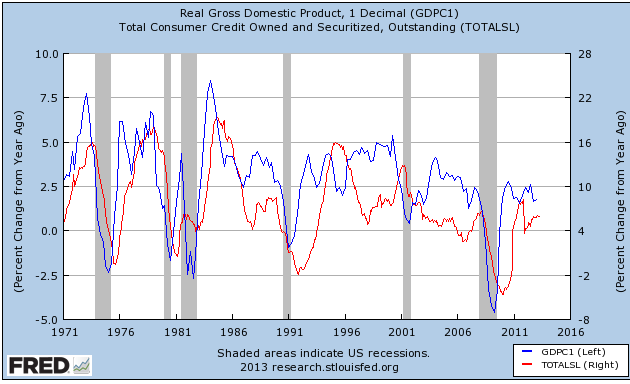

So, increase in interest rates mean increases in total Consumer Credit. So lets look at the relationship between Consumer Credit and GDP (both in YOY % change):

Almost identical…increasing Consumer Credit correlates to increasing GDP

This is the old geometry problem. “if A = B and B=C then A=C”

Now, we can get into a chicken and egg argument here, is is higher GDP, leads to higher Consumer Credit leads to higher rates or is it higher rates leads to higher Consumer Credit leads to higher GDP? We can probably argue all day/month/year about the order but it is true either way, higher rates do not automatically decrease Consumer Credit and then GDP, in fact the opposite generally is true, they rise/fall in tandem. Were it true that higher rates automatically decreased consumer credit and GDP, these chart would be moving contrary to each other, not together

Let’s look at what the rise in rates really means:

The difference in payments on a $200K 30yr loan when rates recently went from 3.4% to 3.9% was a staggering $56/month (sarcasm). At 4.5% the difference is $127/month…..one less dinner out. That is not an amount that will cause anyone to make the “I’m not buying” decision. Further, it would still be cheaper in most areas to buy vs rent until rates approach 10% (see linked article). But, what does that .5% or even a 1% interest spread do for a bank? The difference is very large and it goes more to the rates prime borrowers pay than subprime. When prime bowers are paying 1% or even 2% more on a loan, given their current historically low default rates, that then has the effect of opening up even more credit for other borrowers as the banks are being compensated for the “prime” risk they are taking at an increasingly higher level. Remember, today’s homebuyer has equity the day they walk in the door and as prices rise, so does that equity. This credit expansion has the effect of creating more demand for housing etc and further driving GDP higher. The argument will be that that is an extra $127/month taken out of the economy. Yes, but as the higher rates/consumer credit example above shows, more than that $127 is created from the expansion of credit (money velocity picks up also which also backs this thesis).

This is why you see higher mortgage rates and consumer credit expanding in tandem

Now at times the Fed will step in and artificially rapidly raise rate ( late 90’s). But, and here is the important point, it is done to slow things down. A natural demand based interest rate rise isn’t the harbinger of bad news most claim it is. THAT is happening in response to growing economic activity and is good.

Like everything in life there is a tipping point. Free money (4% mortgage rates are NOT “free money”) will cause activity to increase (though only to a point as this increase is limited to the best credit) and very expensive money will cause it to contract (no one wants it there). But in the middle, if rates are being pulled higher by economic activity, that is healthy not bad….