I will note here that I did reach out to the folks at Saibus last week and did manage to have a conversation last Friday

about their piece. I had hoped that some of the errors contained here would be corrected but they have not. Since I continue to get questions on it, I’m obliged to respond…

The first issue that was brought up was valuation and it contains a critical flaw….

If Howard Hughes can continue its recent run of impressive growth, it could potentially achieve or exceed its prerecession highs of $548.7M in total revenues last achieved in 2006. Howard Hughes’s recent growth in its strategic development asset base is impressive as is its Master Planned Communities segment but we believe that the company is trading at a rich valuation of 2.6X Book Value and 33X TTM operating income

Here is the flaw: Any company that holds real estate is required to hold it on its books at “the lesser of cost or replacement value”. That means a company like

$HHC is required to hold the value of the properties they inherited from

$GGP in its Chapter 11 at a small fraction of their true value.

Two examples:

As of 12/31 the South Street Seaport property that is going to be home to 360k ft of retail space (phase two will add another ~300k sqft) and two condo towers is being held on the books at

$47M (2013 annual report pgs 103-104). Even a little cocktail napkin math tells us 660k sq ft at

$200sq ft and a 5% cap rate (both VERY reasonable assumptions for waterfront NYC retail space) gives us a valuation for JUST the retail section there of

$2B or so… a bit of a far cry from the

$47M “book value” it is being held at . I’ll also note here that we haven’t even touched any potential value for the two waterfront condo towers or any additional development. Not sure how familiar you may be with NYC real estate, but those are gonna be worth more than a little bit. Finally, the

$200sqft assumption for rent is going to prove grossly conservative once things get cranked up there. $400 sqft is wholly reasonable in which case we can say that the Seaport area development is worth ~85% of the current market cap of the entire company at that rent.

Honolulu:

Ward Center is 60 acres ocean front land

$HHC is approved to build 4,000 residential units (condo/apartment towers) and >1MM sqft office and retail space. It is being held at a “book value” of

$370M. Let that sink in.

Sunk in?

The residential first tower, One Al Moana went on sale in December 2012 and sold out 204 units in two days for an average price of $1.6M. So, a property that will support another 3,796 residential units and >1MM sqft retail and office space just sold its first units and will bring at closing

$326M of revenue….is worth

$370M? ……. In order to be using simple book value on

$HHC you have to believe that is true…

Tower 2 and 3 are 80% sold out and Tower 4 has been approved….

We can do this easily…… what would a developer pay for 60 acres ocean front land in Honolulu approved for 4000 residential units plus a huge office/retail component? What would you sell it for?

$370M? I didn’t think so…

The second “risk” they state is oil. This seems to matter because

$HHC has been trading like an energy company in recent weeks…:

One risk to Howard Hughes is the oil and gas markets as the price of West Texas Intermediate oil has dropped 38% since August 2013. Howard Hughes is indirectly exposed to the oil and gas markets because the company will spend $171.5M to build two office buildings that are pre-leased to Exxon Mobil (NYSE: $XOM). Other oil and gas corporate campuses at Howard Hughes’ The Woodlands property include Chevron Phillips, Anadarko Petroleum, and Baker Hughes. In addition, the construction of the Grand Parkway (Texas State Highway 99) will connect Howard Hughes Bridgeland MPC community and its The Woodlands MPC community to ExxonMobil’s new office campus. Howard Hughes expects that ExxonMobil will employ 10,000 at the campus, though if oil prices maintain its downward trend, we expect revenue headwinds for its Strategic Development and MPC business segments.

Let’s go through this. While 10,000 people will be employed there by Exxon, (it isn’t

$HHC saying

this, it is Exxon saying it), the reality is that there will be a total of ~20,000 “workers” there daily (this includes contractors, vendors, ancillary workers, visitors etc). Exxon spent

$1B constructing the campus and has already moved 3,000 people there. There is NO chance it does not get used. In fact they are creating such demand there they have leased the above mentioned building in the Woodlands from

$HHC. The leases are signed,

$XOM needs the space, it is a done deal.

But what about oil prices?

In June 2008 oil hit $145/barrel and then it collapsed to $43/barrel in March 2009 as the “great recession” began……does that drop sound familiar? For reference that drop is roughly 3X the current price retreat. Let’s look and see what Houston home prices did during that time? It only makes sense that if this oil drop is going to hurt Houston and by association

$HHC, we ought to look back at the most recent oil collapse for a guide…no?

In June 2008 the

median home price in Houston was

$174k and the 75th percentile median home was

$291k (it is important because

$HHC is building at the higher end). After oil collapsed $100/barrel over the next 9 months the median Houston home price in March 2009 was

$184k and the 75th percentile median was

$322K*.

Um, that doesn’t make sense….we were just told the opposite was going to happen. Falling oil prices would lead to falling home prices.

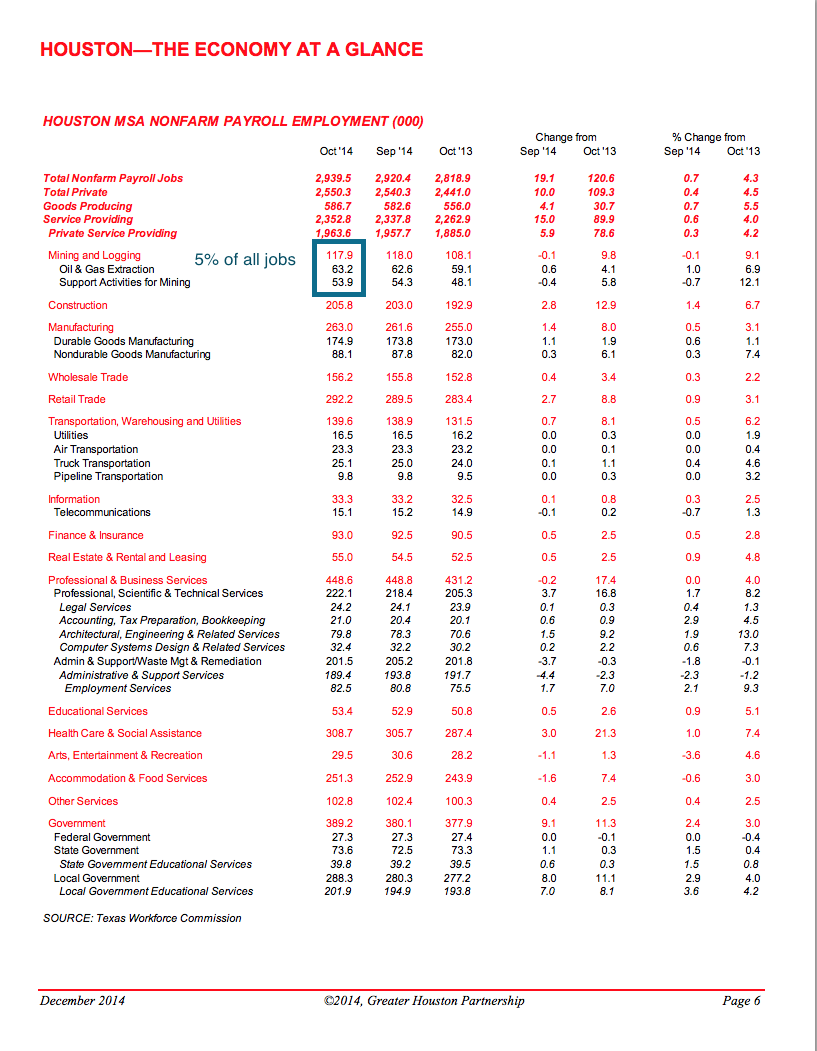

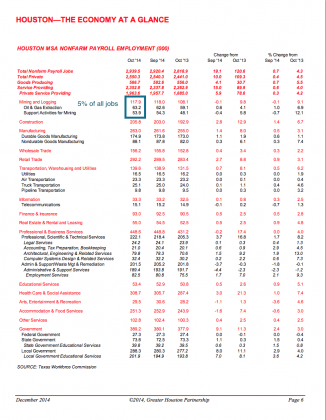

Why then? Well Houston’s economy has made a material shift from its once complete dominance by the fluctuations in oil prices. Below is data from October ’14 from Houston.org. Of the the 2.9M people employed in the greater Houston area, only 118k or 5% are employed in “oil & gas exploration and support activities”. In fact employment there is dwarfed by retail trade, health care, government, lodging etc….

(click to enlarge)

That is why, during the last collapse in oil prices saw Houston home prices rising. People from all professions have been moving to Houston for a decade now both aiding the housing market and diversifying its economy away from the pure oil and gas boom/bust cycle of previous years. Further, should the fall in oil prices cause a cutback in drilling and exploration, that won’t happen in Houston where the HQ’s are. That will happen in places like the Bakken and Utica shale regions causing unemployment there to rise. I am not saying energy no longer matters to Houston, to be sure it does, it is just not as overwhelmingly dominant as it was even a decade ago. Houston now has the largest export port in the US and boasts the world’s largest medical center. Oddly enough, it has been the collapse of natural gas prices that have been a real boon for Houston. Manufacturing to export has seen a surge as low natural gas prices make gulf coast producers competitive internationally.

Over the past decade its population of “college educated residents” has grown in total numbers more the Boston, San Francisco, Silicon Valley and Chicago and Houston added over 400k foreign born nationals, second only to NYC and 3 times the number three city, LA.

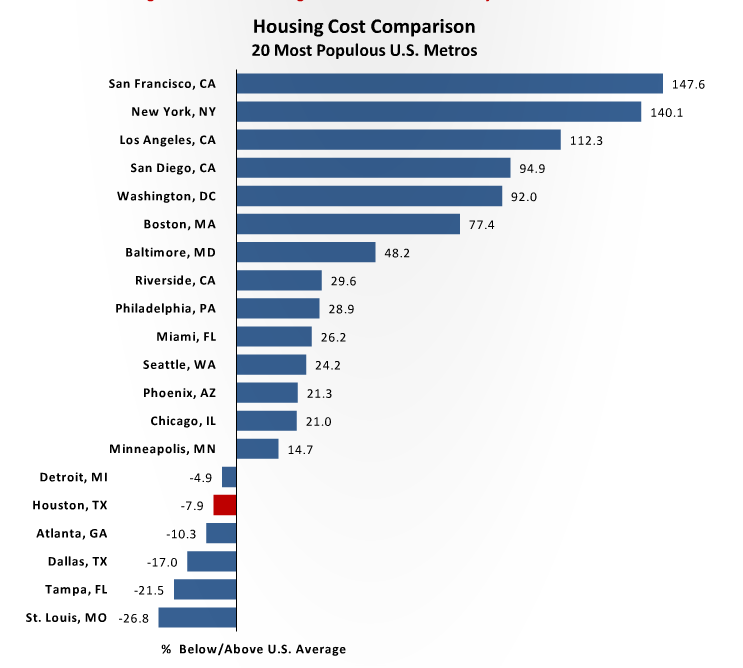

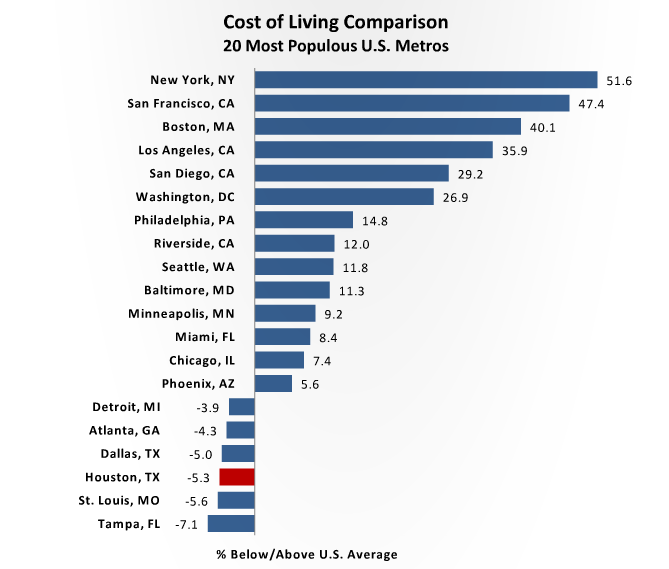

People are flocking to Houston because, despite recent home price appreciation, both housing costs and cost of living are far below other major metropolitan areas:

What does that mean? It means there is going to be constant embedded demand for housing and retail in Houston as its low cost of living continues to attract people from all over the world and a drop in oil prices will not derail that. More important to Houston now is a recession than a drop in the price of oil. Since no recession is on the horizon and falling energy prices help make that even more remote, we can further state Houston should be little affected (if at all) by a short term oil fluctuation.

Further, the Woodlands is almost built out from a residential perspective. What they do have is the potential from millions of sqft of commercial and retail space they can build. For reference, The Woodlands is the size of Manhattan. Bridgeland, the “sister MPC” to Woodlands only started selling lots this spring of 2014 and will receive as huge tailwind in demand once the above mention highway is completed as it essentially connects the two MPC’s:

In the second quarter of 2014, we received bids from homebuilders for the sale of 509 lots at an average price of $90,000 per lot, or approximately 17.4% higher than the average finished lot prices during 2013. We anticipate the pace of our future lot sales will increase because we are able to develop and deliver a much higher volume of finished lots compared to 2013 and the first six months of 2014 since obtaining the wetlands permit. As of September 30, 2014, Bridgeland had 344 residential lots under contract of which 266 lots are scheduled to close in the fourth quarter of 2014, providing an estimated $27.0 million of revenues. The remaining 78 lots are scheduled to close in 2015, providing an estimated $3.6 million of revenues.

Neither is in any danger of seeing demand for their MPC’s slowing at all due to oil price declines. Unless you are of the opinion the “new normal” in oil is well below $60/barrel, then our current pricing level is temporary and thus its potential impact is negligible if any. But to be thorough, lets assume homes price do fall 20%. Given the diversity of their asset base, what effect would that have? Remember, if oil prices fall and crimp the pocketbooks of Houston residents, that same fall grows the pocketbooks of residents in Vegas, NYC, Columbia MD, Honolulu, Virginia and New Orleans where

$HHC also has properties. Further, our 20% fall in home prices scenario is far worse that what was seen during the “great recession”

From Compass Point Research (reprinted with permission):

HHC’s NAV: Exposure to Energy

HHC’s Houston-related assets comprise $62 of our $210 NAV: 1,007 acres of Woodlands saleable land which contribute $7/share, 4,566 acres of Bridgeland saleable land which contribute $11/share, and the

$3B in commercial developments both under construction and planned for development at The Woodlands’ Hughes Landing, Town Center, and Resort & Conference Center which contribute $44/.

If we immediately cut land prices at Woodlands and Bridgeland by 20%, raise stabilized CRE development cap rates by 100 bps, and push out all future developments by 2 years, our NAV drops to $192. If we then push out our NAV by one-year to 2016, it rises back to $216 PT. Thus, as it currently stands, the time value embedded in HHC’s NAV fully offsets what we believe is a fairly draconian scenario in which Houston land values plummet 20%, all developments are pushed off two years, and CRE stabilized valuations drop roughly 15% (from a 6% cap to a 7% cap).

Think about this, currently the company produces ~

$70M NOI across its portfolio from its operating companies (excluding land sales). In 2015 Summerlin Center will increase that by ~

$40M and we can add another

$5M -

$10M from a host of additional properties coming online next year (could be more, depends on timing, if not, they roll into ’16). So, in 2015 NOI is up 50% to 80%. Then the Seaport is finished Q3 or Q4 2016 and about a dozen other operating properties (that we know of, I fully expect more to be announced between now and then) come online and NOI jumps again to ~

$200M/yr in 2017. That is some serious growth

This all ignores operating properties in Ward Centers when they come online (not many announced yet) and any monies from land/residential sales along the way (like a few thousand waterfront condos in Honolulu/NYC).

Additionally, the company is financing its massive expansion without the use of corporate level debt (they are using property specific non-recourse debt). Earlier this year they issued

$750M in Senior notes. How much of that has been used? $0. The company is sitting on near a billion dollars (

$809M) of available funds just waiting for a use….

When we hit

$200M in NOI, then it is time to spin the operating properties into a REIT or buyback a huge amount of stock or make a large acquisition. My thought since the day

$HHC was formed was the REIT spin so I will stick with it.

Any pullback in

$HHC is a huge buying opportunity for investors

*(Skeptics will argue Houston home prices did fall in 2010-11 but that was not due to oil prices, oil then was back from $40 to the $80-$110 range. Houston home prices dipped slightly then due to the national housing collapse and even then the drop was a small fraction of what happened nationally and their recovery to previous levels was rapid.)