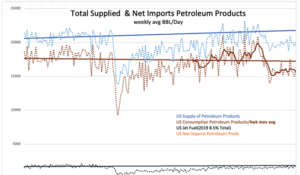

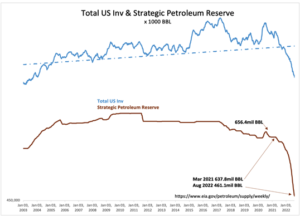

I’m stunned the inventory numbers aren’t concerning more people. We are getting to levels where a singular event could cause major disruption to the economy via oil prices making another large leap higher. I’m talking $70-$100 bbl more, not $10-$20. If the first chart on the left below doesn’t scare you, you’re not reading it correctly.

“Davidson” submits:

- US Total Crude Inv declines 10.5mil BBL(a decline in working inv of 7mil BBL and decline in SPR 3.5mil BBL), US Crude Prod declines 0.1mil to 12,1mil BBL/Day, US Crude Imports decline 1.3mil BBL/Day(9.1mil BBL/Week), Fudge factor is 0.699mil BBL/Day(4.9mil BBL/Week)

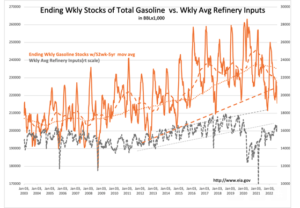

- US Gasoline Inv decline 4.4mil BBL, Jet Fuel and Diesel remain mostly unchanged as do US Exports of Refined Prod, US Refinery Inputs decline 0.3mil BBL/Day

The declining trend in inventories continue. US Export and Domestic consumption continue. Some in the media express alarm at the building supply/demand imbalance with markets dominated by algorithms ignoring fundamentals. It is clear that new relationships are occurring between consumption vs inventories. At some point, the current trend vs global expansion will prove a concern, but not today. Perhaps Oct 2022 will be a turning point should the US reverse SPR releases and turn to rebuilding inventory but predicting turns in political agenda should not be part of one’s investing timeline. Fundamentals support owning this sector for the long term when realities of energy sources, their respective effectiveness, utility and etc will prove out where the better economically viable lay. My opinion is that traditional fossil fuels will remain the major resource it has historically.