“Davidson” submits:

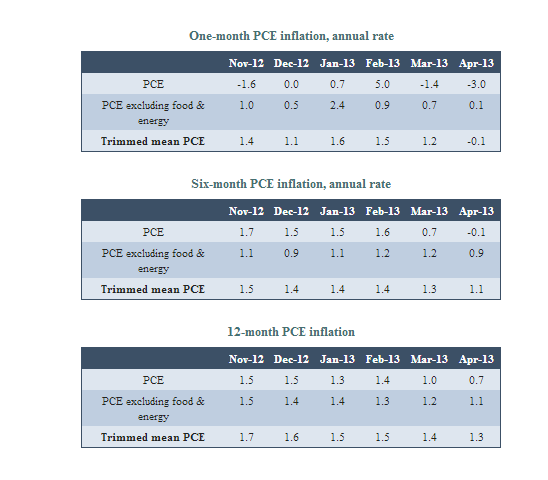

The Dallas Fed released its 12mo Trimmed Mean PCE core inflation measure at 1.3% for April 2013-see the tables below. By combining this inflation measure with the long term US Real GDP growth rate one gets the “Prevailing Rate” which is ~4.32%. Using the Prevailing Rate to capitalize the long term earnings mean earnings for the SP500 ($79.64) ($SPY) one can calculate the SP500 Intrinsic Value Index at $1,848. This is a dynamic calculation in that mean earnings for the SP500, core inflation and Real GDP change over time. History of the SP500 Intrinsic Value Index from 1978 reveals that the major market lows during recessions correlate well this index. The SP500 Intrinsic Value Index is also the market level at which the very good value investors, i.e. Warren Buffett, Wilbur Ross and etc, have found the equity markets attractive.

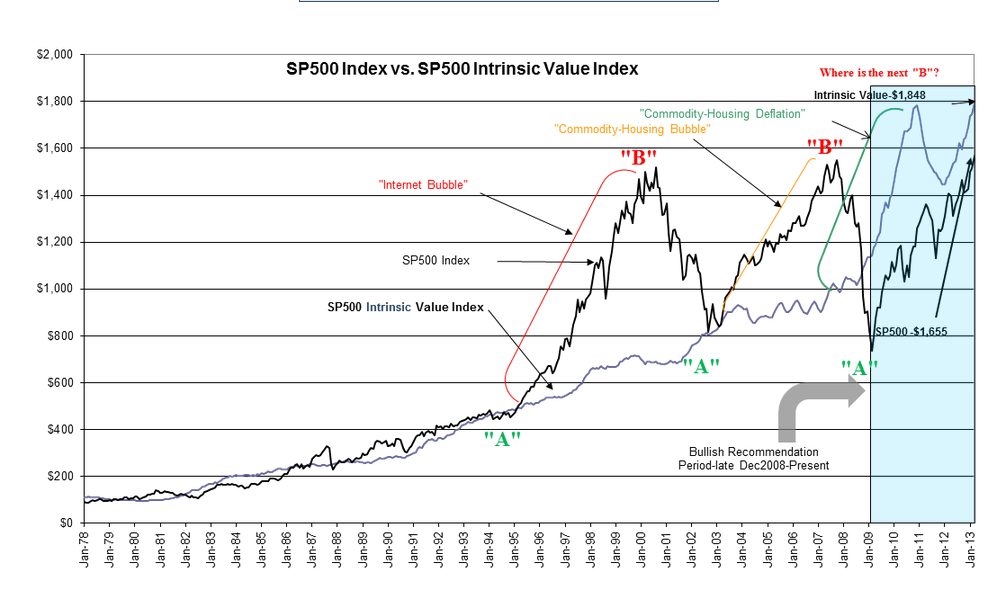

The SP500 remains slightly more than 10% undervalued vs. the SP500 Intrinsic Value Index.

Lower inflation results in higher market valuations over time all other things remaining equal. The history of inflation and SP500 P/E reveals that lower inflation results in higher P/E levels while higher inflation produces lower P/E levels with a lagging investor response of ~3yrs called “The Recency Effect”

If one reviews the trends in the PCE data, one can anticipate that for the next few readings that inflation is likely to head somewhat lower which in turn results in higher levels in the SP500 Intrinsic Value Index. For equity investors, falling inflation has always provided higher equity prices historically and we can expect a similar impact this time in my opinion.

The history of the SP500 Intrinsic Value Index indicates that since Hedge Funds emerged as a significant market influence in 1995 more recent major market tops have been at 55%-100% in excess of the index. These major market tops have coincided with peaks in economic activity, i.e. peaking light vehicle sales and employment levels. The economic data continue to reflect economic expansion which is likely to last, again based on historical records, 5yrs-6yrs into the future.

It is my opinion that we are likely to experience a market overvaluation as we have in the past 2 market tops. The timing and the pricing of the next major top are unpredictable, but we can monitor economic activity and tell when economic activity is slowing significantly. Till that time arrives, investors should maintain a strong commitment to equity in my opinion.