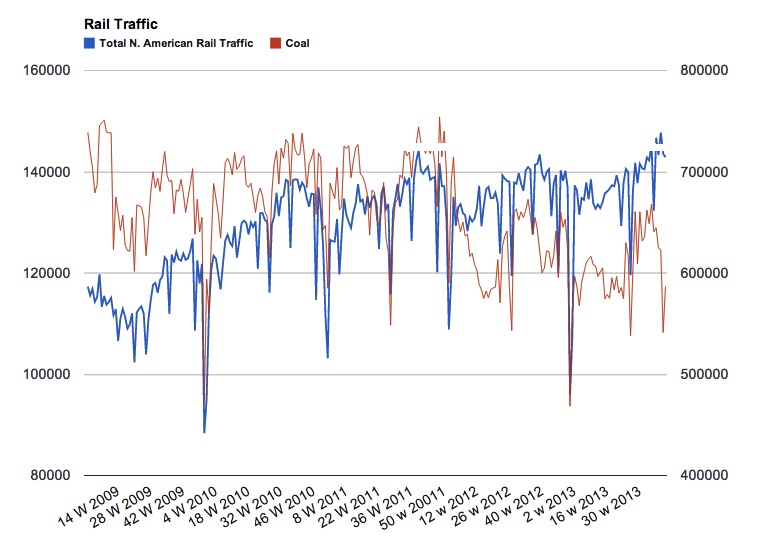

Total N. American rail traffic came in at 714k carloads last week, comfortably ahead of last year. All categories Saw nice YOY gains except stone & related products and grains saw minute declines. Coal of course continued its declines but that is expected..

Here is the chart:

I should note that the 714k carloads while is just slightly below the high level from last year and the drop in coal YOY accounts for the difference. That gives us three straight weeks where N. American rail traffic has met/topped the highest level from last year.

Now, we are not crushing the numbers which tell me that we will see economic growth continue albeit at a less than stellar pace. I would not get too excited/depressed over the early earnings reports. The banks ($WFC, $BAC) were good and $JPM was decent ex the litigation issues. It is too early to tell where things in general will end up as Q3 comes in but I think we’ll see more of what we saw the first half of the year.

The one area that might get hit would be the retailers and consumer confidence fell in early October due to the incessant BS coming out of Washington. Those workers who were furloughed more likely than not were notified well ahead of the actual event and would have adjusted their spending in Sept in anticipation. Furloughed workers I’m gonna go out on a limb and say were not buying anything but the essentials and a host of other folks who feared a prolonged shut down and/or possible default would have correspondingly retrenched.

I’m thinking a decent amount of that comes back eventually but I am not sure it happens in the next two weeks.