“Davidson” submits:

There is myth in political thought and Central Banker thinking that lower mtg rates will be inflationary. This is not in fact true. It should be clear that lower mtg rates, i.e. narrower credit spreads globally is DEFLATIONARY

If lending institutions cannot lend profitably, then they will not lend, duh!

A credit spread wide enough to satisfy the historical need for financing we have enjoyed for 100s of years is not present today. This has been in part due to Central Bankers jawboning mtg rates lower and actually buying longer term maturities with issuance of govt debt. This is deflationary as those lower on the credit ladder cannot borrow and cannot even refinance at lower rates.

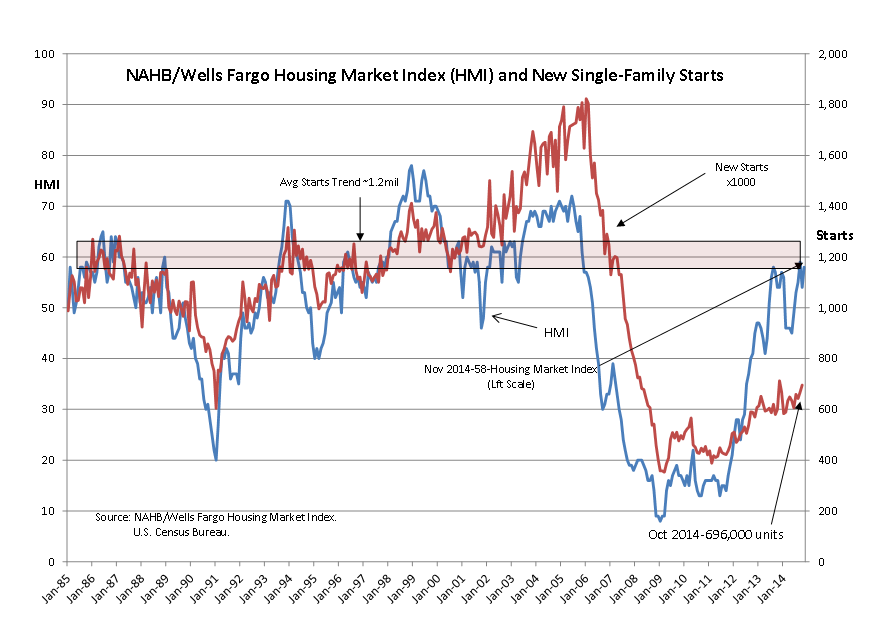

Housing, commercial construction and the flow of non-professionally trained individuals into middle class income levels occurs with a much more vibrant lending environment than we have to day. The MCAI(Mortgage Credit Availability Index) shows we remain at very low credit issuance levels as do Single-Family Starts and Construction Employment trends. Central Bankers do not show they understand how economic activity is connected to credit availability.

Doesn’t anyone get it: Low Lending Spreads = Deflationary Environment

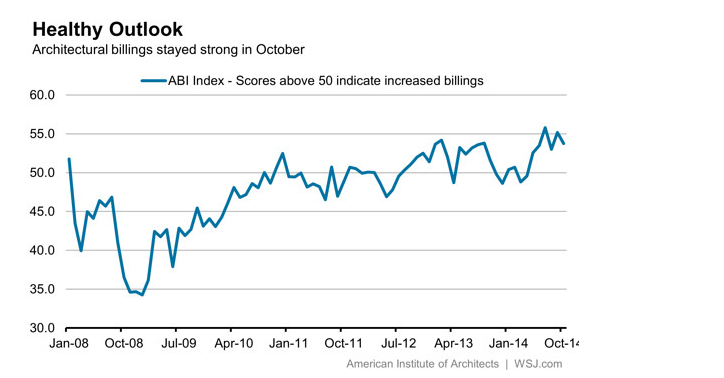

The architectural billings index came out today and while backing off the previous record number, the index is solidly in the “growth” mode meaning increased construction in the coming months.

Billings by architecture firms remained strong in October thanks to continued activity by developers of rental apartment buildings as well as new demand from such institutions as schools, hospitals and municipal governments, according to the American Institute of Architects.

The Institute’s monthly Architectural Billings Index hit a score of 53.7 in October. That was down from 55.2 in September, but any score above 50 indicates an increase in billings, according to the institute. October was the sixth consecutive month that the score was above 50.

Billings were particularly strong in the west and southern regions, but the index for the northeast declined to 47 from 49.8 in September. The index’s commercial/industrial category saw an increase to 52.3 from 51.5 in September. Residential clocked in at 54.7, down from 55.1 the previous month; and the institutional sector stayed steady at 54.4

As for single family starts ($XHB), the uptrend continues with Oct coming in at 696k starts and September revised up 22k to 668. Neither are blowout numbers but yet more indication of the steady growth we have seen for the past few years.