This is from my comments on their Seeking Alpha article……

I am not going to respond to this in a post. I’ll only say here that any analysis of CRE properties that uses stated BV as a valuation metric is irrelevant on its face before anyone reads any further. In order to use it, the assumption has to be the properties are only worth their cost to the owners. If that is so,,,,,why build anything? REIT’s do not trade on BV or PE, $SPG trades 11X BV (41PE), $GGP 3X BV (57 PE), $TCO trades 11X BV, $MAC trades at 3.5X BV (53 PE).

By any of those comps, $HHC is a steal at current prices…

Okay….I changed my mind… I am going to post

Think about it, stated BV for most properties is its cost (the lesser of cost or replacement value). So, if its true value was only its cost, why would anyone ever build anything? There is no economic incentive to build something in which one only gets their cost returned. The return on the asset and the effort to build then is effectively zero. If that isn’t true then (it isn’t) then what rational person would attempt to value that property on simply its cost?

If Saibus is going to use the stated BV of $HHC’s operating properties as a valuation metric, even if it is wrong and they are being fair then they have to use that valuation in regards to how it compares with others in the space. Right?

So, sure….lets value $HHC on stated BV with peers like above and give it a “value” of 11X BV or over $500/share…lets go lower at even 5X BV or ~$250/share

Yes, I know that makes very little sense…just like saying it is overvalued now for the same reason does…..

Maybe $HHC deserves a “discount ” to that because of its alleged (I say alleged because there has been no data presented to prove the claim) oil sensitivity? Does it deserve a 73% discount in valuation (2.6X BV vs 11X)? Well then shouldn’t $SPG also get a “discount”? It has 25 properties in Texas (making it the largest) as well as 8 in Japan (in recession) yet clearly is one of the most “expensive” properties in the space based simply on BV and PE. No discount there? Just maybe this oil thing isn’t that big of a deal?

Some will respond and say, $HHC isn’t technically a REIT currently. This is where folks have to have actually done some deeper research on the company. $HHC emerged from the $GGP chapter 11 with ~$400M of NOL’s on their books. Being a C Corp now allows them to shelter their income from operating properties and land sales via the NOL’s and plow that savings back into the company for its current expansion (this is why they have expanded so fast with so little debt). Where they to opt to become a REIT now, the corporate change would cause them to lose the NOL’s & they’d have to pay out their profits to maintain REIT status. That would be irresponsible.

They are rapidly using their real estate asset base to develop a large array of income producing real estate properties……sounds like? Starts with a “R” ….ends with a “T”…??

Let’s take it a step further, let’s take a hard line and say “$HHC isn’t a pure REIT so we can’t value the whole thing like other REIT’s”. I know, it is odd but play along… So let’s look at only the operating properties that would be a REIT comp and ignore everything else…that’s fair, right?

From Saibus’ piece:

Although we conclude that the current carrying value of Howard Hughes’s assets is not significantly undervalued….

So, they claim stated BV is a “fair value”

Ward Villages $370M BV, 11X BV comes to $4B valuation

Seaport: $47M BV, 11X that comes to $500M

The total Market cap of the company is $5B. This means these two properties are worth nearly its entire market cap (using only their own valuation). This also means we now get all the land in Summerlin, The Woodlands and Bridgeland for free. It also means all the commercial development in those areas is valued at essentially zero and gives no value to the Columbia MD, Alexandria and New Orleans properties and the condo projects in Honolulu. If you only want to use 5X BV go ahead, you’d only have to toss a few of the “freebies” listed above to get to the $5B and still have plenty left over. OR, you have to believe this list of unleavered properties actually has a negative value.

If we value these the correct way: Downtown Summerlin and its $40M normalized NOI at a 5% cap gets us a ~$800M valuation of just the retail section that is open. The soon to open office tower and luxury condo tower will only add to that. The Exxon towers Saibus references will produce ~$12M NOI, we will give that a 6%-7% cap since it is office space so they are worth ~$200M giving us $1B in value from just those two projects. The currently in operation operating properties will produce ~$70M in NOI in 2014 (this excludes Seaport), take a 6% cap and they are worth ~$1.2B for ($1.4B at 5% cap) ~$2.2B total. We still haven’t even talked about a single home site sale, the Westin and Embassy hotels they will run and the near two dozen other operating properties (only counting those that have been announced) coming online in the next two years and everything else from above (Ward Villages, the Seaport, Hawaii condo sales etc etc etc ).

Let’s look at the other metric they use, PE ratio. While $HHC sports at PE of 29X (their number), the above comparison companies sport PE’s in the 40’s and 50’s. So sure, let’s use it and ratchet our “value” up over 60%-70% to match its peers PE ratios.

Yes, I know it makes little sense to do that also……I’m making a point here…

I have no problem with someone saying “I think the Seaport and Downtown Sumerlin are going to produce 50% less NOI than you expect and should have an 8% cap rate, not 5% or 6% and for that reason think they are worth less…..”. At least they are valuing the assets the right way. Reasonable people can debate NOI and cap rates give reasonable data to back those assumptions…..

What I DO have a problem with is using valuation metrics wholly inappropriate for the asset class and then using that metric to come to a valuation. Further, I DO have an issue with then taking that valuation and not even bothering to take a look and say, Hmmmm, I wonder how my valuation compares to other companies in the same space. If you insist on using BV and PE for valuation, they you at least ought to see how other RE companies trade in correlation to them also…….

The perversity of their own analysis is that it shows the company is drastically undervalued in comparison to similar companies, not overvalued.

They do say:

Although our firm managed to have a conversation with him….

They make it seem as though I grudgingly agreed to talk to them. Reality is I requested the call (a couple times) to give them a chance to correct some items before I wrote anything and even then waited some time before responding. Further, the analyst responsible for the article opted out of the call despite the time of it being at their choosing. Instead what happened was another piece expanding on the previous errors

Finally, they seem to be doing a bit of a victory lap due to the recent fall in price in $HHC, as if it justifies their analysis:

At least Howard Hughes’ share price has declined by 9.6% since we published our article and 18.5% since it closed at its all-time closing high of $160 on August 19.

They may or may not be doing a victory lap but why include it if they aren’t? They do omit that shares are still up 17% last 12 months but we’ll ignore that. Let’s assume their article is 100% directly responsible for the recent price fall and it has nothing to do with the market turmoil of the past few weeks. In the short term, anything can happen for any reason, right?

If they are responsible, it isn’t hard to imagine why, it is a pretty simple recipe, intentional or not:

1- Take a small underfollowed and thinly traded company that is hard to understand and value

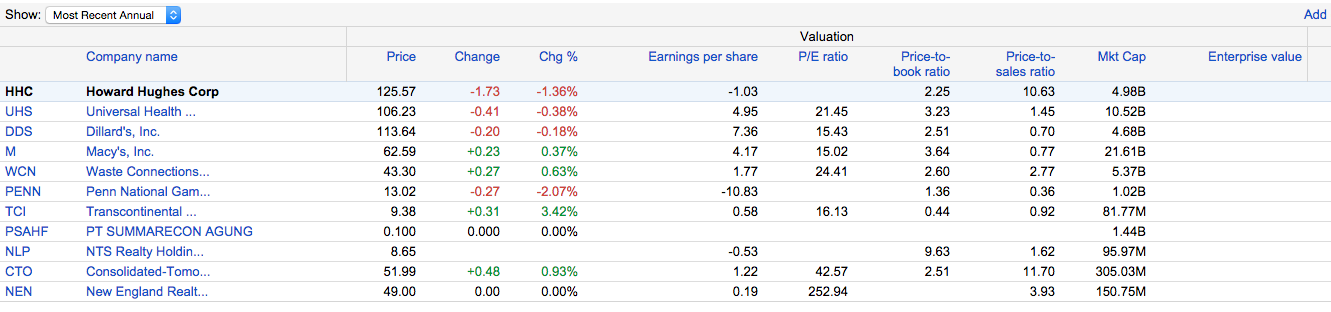

2- Make sure even major finance sites do not know how to classify it (based on stated “competitors”):

Google Finance does not know if it is a REIT, retailer, energy co or gaming co….

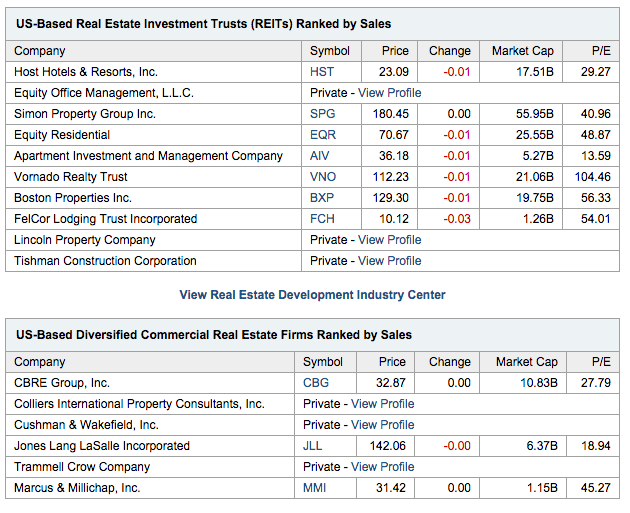

Yahoo Finance at least keeps in mostly in the RE space although they pretty much hit every possible segment (office REIT, apartment REIT, developer, hotel operator, retail REIT etc)

Seeking Alpha says straight REIT

3- Take whatever is spooking markets at that time….in this case oil…

4- Apply #3 to #’s 1 and 2 using tenuous logic unsupported by any data whatsoever that might prove/disprove the claims…

5- Make sure to make valuation claims using metrics not used to value companies in the space by any research firm and without basing that valuation call in comparison to similar companies.

6- Publish on widely read website…

Presto…….

I’ll simply say what I said before, for those looking past the rest of 2014 and into late 2015 and 2016, shares offer compelling value here……….