“Davidson” submits:

One of the strongest themes in our markets is that not only do many believe price trends forecast the direction of economies but that price trends actually direct economic activity. My analysis(which I have often repeated) indicates that it is economic activity which eventually translates into stock prices by impacting market psychology. The formula is fairly simple but not precise.

1) Rising Economic Activity = Positive Change in Market Psychology = Higher Equity Prices/Lower Bond Prices

2) Falling Economic Activity = Negative Change in Market Psychology = Lower Equity Prices/Higher Bond Prices

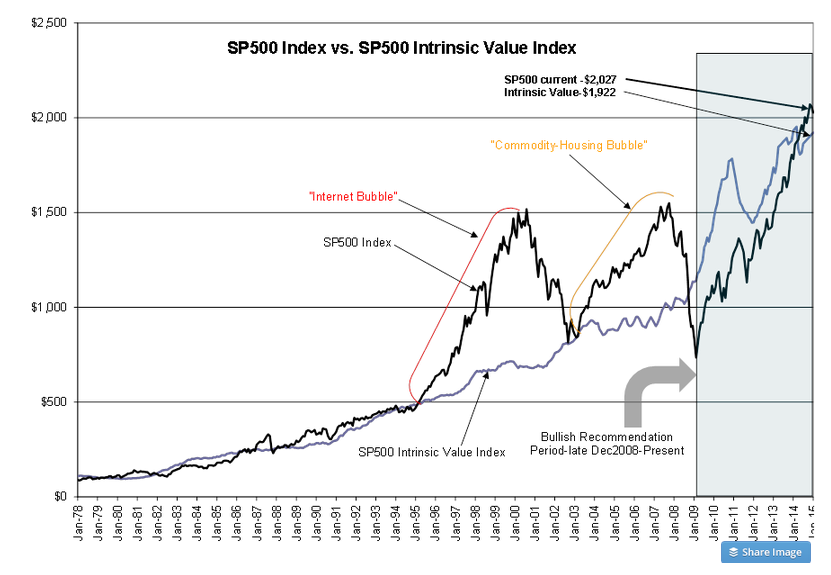

It is relationship between Economic Activity, Market Psychology and Market Prices which has been the mystery of the ages. So many, get it so wrong that we have witnessed considerable swings since 1995 when Hedge Funds began to dominate (when Hedge Fund capital rose over $500Bil) the short term price swings in market prices.-see Chart 4: SP500 Index vs. SP500 Intrinsic Value Index. 1995 and beyond we have witnessed considerable market volatility not seen previously. We can see the increase in volatility using the SP500 ($SPY) ($INX)Intrinsic Value Index for comparison. I cannot explain it all in a short note which requires detailing how various investors’ perceptions determines their market psychology, but the short version is ‘Value Investors’ buy using long term GDP for valuation and create the market lows(this is the basis for the SP500 Intrinsic Value Index) while Momentum Investors invest using price trends and news headlines. Hedge Funds are responsible for market excesses-highs and all the volatility in between.

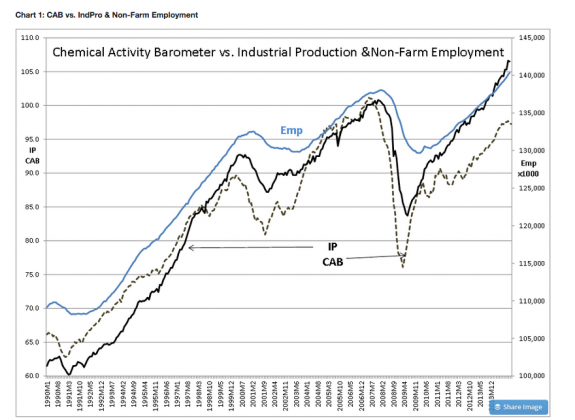

This week we had the Chemical Activity Barometer(CAB) and New Home Sales (from which comes the Monthly Supply of New Homes for Sale)

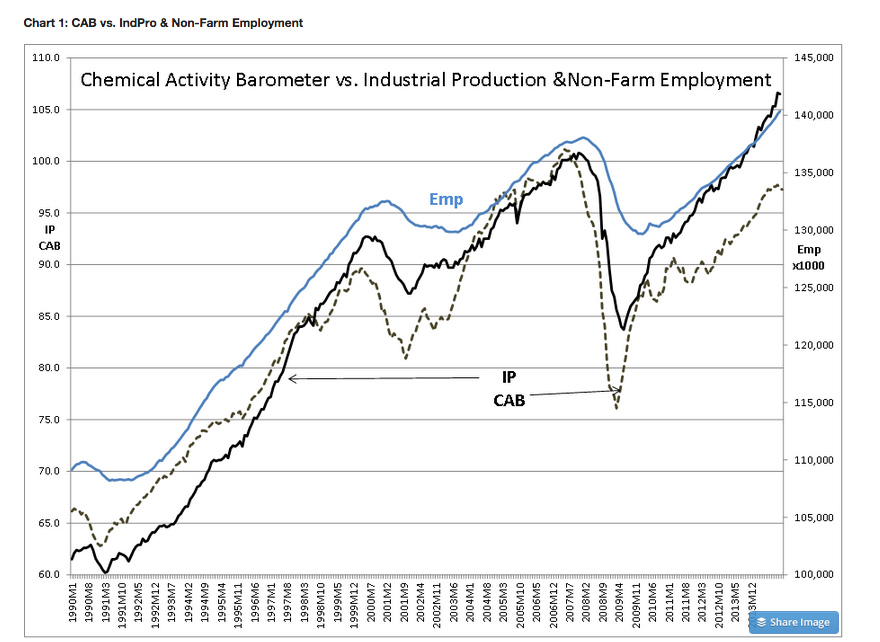

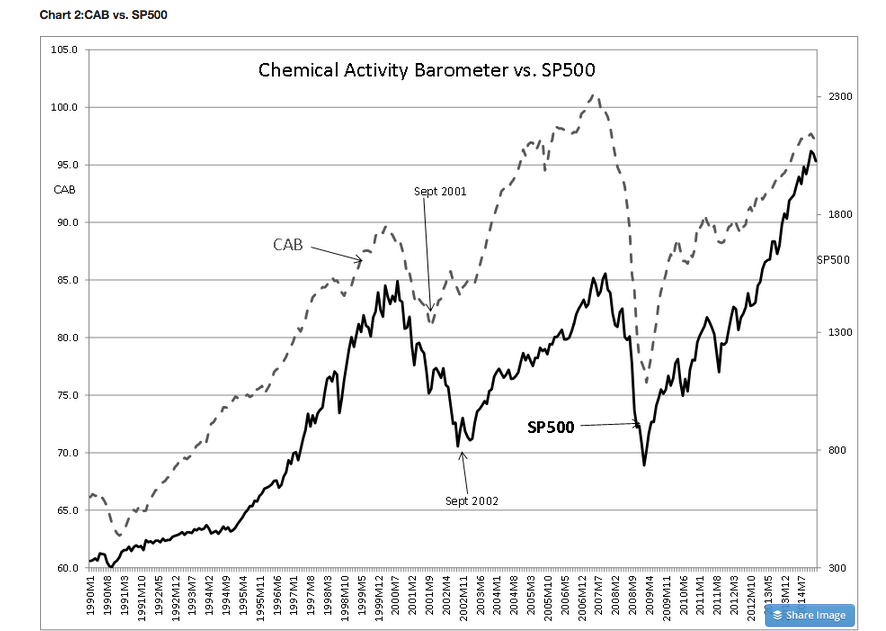

The CAB has a long history of correlation with economic activity-see Chart 1: CAB vs. IndPro & Non-Farm Employment. For this reason turns in the CAB are good at helping to identify levels for buying and selling the major turning points in long term SP500 investment cycle(Not at all helpful for temporary changes in market psychology)-see Chart 2:CAB vs. SP500. The current report continues to support a positive economic outlook. While it may look like the CAB is topping, previous reports have been revised higher. Today’s report is positive!!

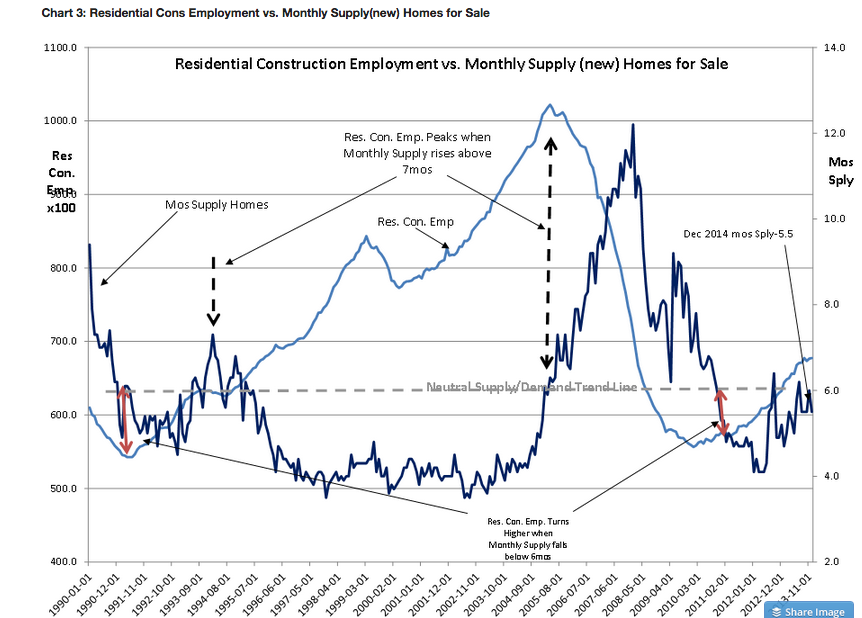

New Home Sales data was surprisingly good. New single-family home sales boomed 11.6% in December to a 481,000 annual rate, coming in above the consensus expected pace of 450,000. Sales are up 8.8% from a year ago. This report translates to the more revealing Monthly Supply of New Homes for Sale which I correlate to jobs in Chart 3: Residential Cons Employment vs. Monthly Supply(new) Homes for Sale. Construction remains the lagging sector of our economy. I identify the Fed’s keeping mtg rates low as the reason why Single Family Home Sales remain well below historical norms and the cause for less than historical employment gains. Unskilled workers, more often than not, enter our economy via construction markets. They gain skills and eventually make good incomes during construction cycles. This is how their children eventually enter professional jobs and the ‘middle class’ grows. This recovery has not had a normal construction cycle rebound due to the Fed’s keeping mtg rates low which does not provide enough of a credit spread to permit banks to lend to FICO scores less than 720-740. Just the same, there has been an influx of global capital willing to accept lower returns in exchange for a capital safe haven. This is one of the reasons for our strong US$. The other more dominant cause in my opinion is Hedge Funds.

In 2010-2012 Hedge Funds were often in the media explaining that they had made considerable bet on ‘hyperinflation’ due to Fed liquidity actions. They shorted the US$(a bet that rates would rise), bought commodities especially oil and copper, shorted the 10yr Treasury and even bought farm land causing prices to double. In 2012 we had ‘Peak Oil’ fears to help fan the flames. What few paid attention to was the ‘fracking revolution’ which was already producing oil in unheard of amounts from previously unproductive sites. EOG’s Mark Papa and Continental’s Harold Hamm told us at the time that considerable production was on the way, yet Hedge Funds bet for much higher energy prices. Having this ‘hyperinflation bet’ in place, Hedge Funds were solidly on the wrong side when Russia invaded Ukraine. The US$ began to strengthen and the 10yr Treasury yield fell as Russian capital along with other global players turned to the US as a safe haven. In June 2014 oil prices which were part of the ‘hyperinflation bet’ began to weaken and the volatility we have just experienced is the net result. Many things have been in the media: Saudi raised its production, the US production created a ‘glut’ and etc. If one examines the EIA data, some excess production occurred but nothing greatly out of line with history. In fact oil production has fallen relatively sharply from Oct 2014 due to price declines and we could be in the position of excess consumption today. The next EIA report is Feb 11, 2015.

I lay the rapid price changes on Hedge Fund activity. Fundamentals did not justify such dramatic shifts in currency, commodity prices which also impacted securities. For a fundamentalist, this presents opportunity in which I recommended shifting assets from high priced SmCaps to better Reward/Risk assets such as LgCap Domestic and International as well as Natural Resources. I expect that normalization of the US$ should occur. It may occur as quickly as it strengthened. Such a rapid reversal is not unprecedented, we will just have to wait and see. Hedge Funds who were net long in August are now net short-fundamentals do not change that quickly.

Yes, market prices are pure market psychology with some investors judging changes in psychology or valuations better than others. If market valuation had a mathematical solution we would have had it long ago. We have some very good managers. I expect them to do well for us.