There is still significant upside to housing starts…….higher rates will help boost housing….

“Davidson”submits:

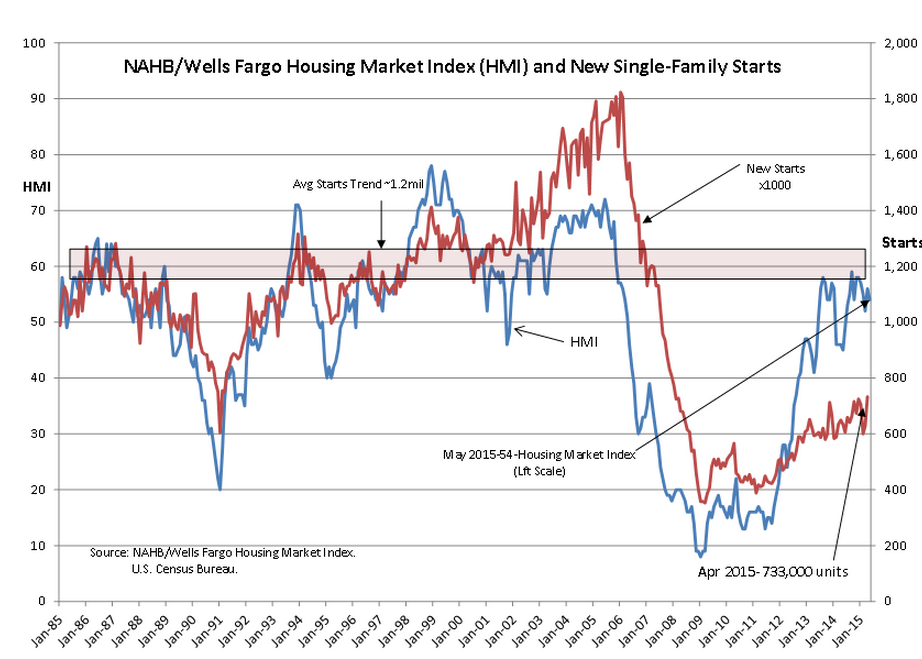

The NAHB HMI(Housing Market Index) and Single Family Starts were reported the past two days. The HMI ($XHB) at 54 and Starts at 733,000 indicate that a positive trend remains in place. Many appeared to have been surprised by this and talk of a 20% rise in Starts. But, if you look at the chart below, you will see an uptrend created by choppy monthly reports. That the uptrend from early 2013 simply continues is all that one can say at the moment.

Historically Starts have averaged at ~1.2million range. There is still considerable room for Starts to improve. Home buying relies on bank lending. Bank lending relies on the spread between cost of funds and return on mortgages. Higher 10yr Treasury rates on which mortgages are priced while T-Bills remain roughly where they are will give banks the spread they need to broaden mortgage lending.

One of the myths often repeated is that higher rates slows economic activity. The facts are a little more complicated but easy to understand. Banks require sufficient spread between the cost of funds and the rate of mortgages to cover expenses and future liabilities before they can lend. The wider the spread, the greater the risks lending institutions are willing to take. In the current economic climate, lending has been limited to wealthier borrowers because there is less chance of default. Wealthier borrowers put up more collateral than the average borrower which reduces the risk to banks. While mortgage rates of less than 4% sound attractive, most cannot participate due to strict requirements on income, down payments and collateral. Low rates do not boost lending! Low rates do not stimulate the economy! What is required for wider lending is a wider spread. In the current climate, I estimate that mortgage rates in the 5%-6% range would make banks more willing to lend.*

*Since mortgages are priced 160bps off the 10yr Treasury rate, then we should cheer for a rise in 10yr Treasury rates while T-Bill rates remain roughly the same. A 4%-5% 10yr Treasury rate with T-Bill rates remaining mostly unchanged would stimulate housing, employment and our economy.

The Fed’s history indicates that it generally does not control rates. The Fed has most often followed the T-Bill rates. It is market forces which control rates as investors seek higher returns. The rising rates we are seeing today may be part of this shift. If so, it would mark a significant change in investor psychology and a positive for equities.

Brian Wesbury comments:

In the twelve months ending in September, 35.8% of all housing starts were multi-family units, the highest since the mid-1980s. Now that share is down to 34.9%. That’s significant because the construction of a single-family home usually adds more to real GDP growth than a multi-family unit. Based on population growth and “scrappage,” overall housing starts should rise to about 1.5 million units per year over the next couple of years, so a great deal of the recovery in home building is still ahead of us.