“Davidson” submits:

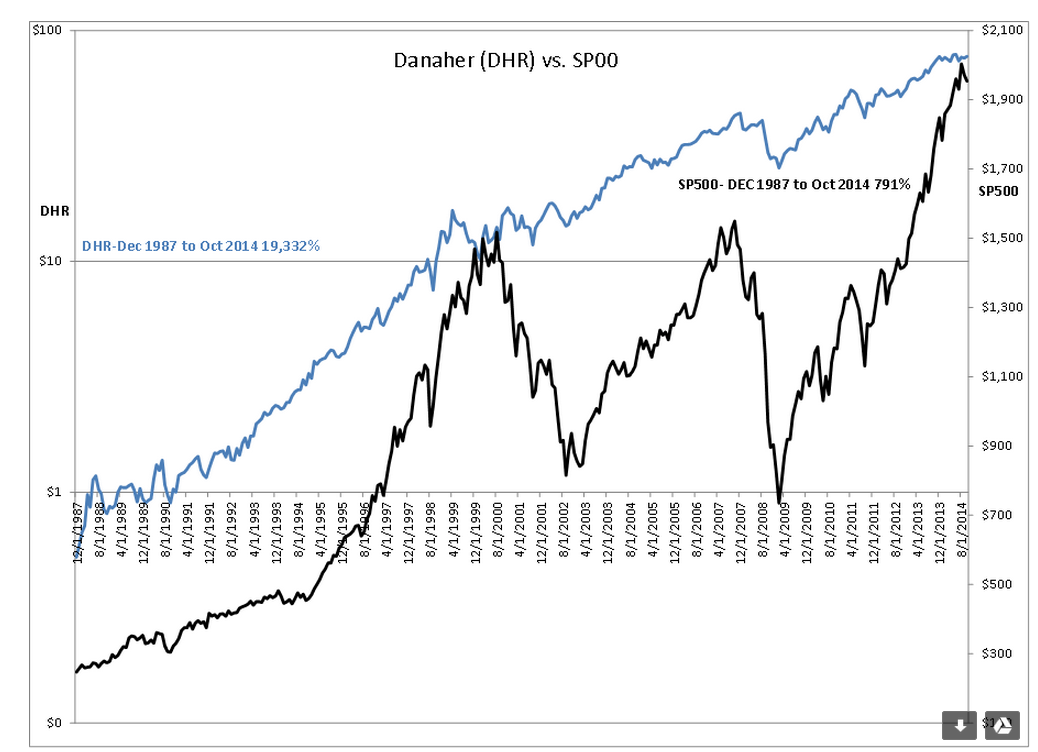

Danaher’s share price has risen an extraordinary 19,000%+ from Dec 1987 compared to the SP500’s ~800%-see chart. This begs the question, “What drives stocks over the long term?”

The best parameter I can find has been one mostly ignored by scholars and investors in the past. I say most ignored, but a few seem to get it. Most today will tell you it is one of the often discussed parameters-per-share ratios prominent in the media, i.e. Revenue-Cash Flow-Free Cash Flow-Earnings or some other business measure on a per share basis. With Internet related issues the parameters measured are ‘clicks’ and ‘eyeballs’. There is always some measure and many times differing measures offered by analysts to justify their belief in pricing a certain business in a particularly hot sector of the market. But, many of these do not hold the test of time. By ‘test of time’ I mean at least a couple of business cycles. Many Internet related issues seem to last only a few years before being pushed aside by a newer, better and faster ideas. All of us have witnessed issues which soared to many multiples of revenue (without earnings) before evaporating investor capital as they failed to deliver on promised earnings.

Danaher ($DHR) which has stood the test of time is in my opinion a good example of what holds value over time. The one parameter which differs in all companies which have done well vs. those which have not in a study I performed on the SP500 ($SPY) was the growth of shareholder equity, i.e. Book Value(BV). Companies can have revenue growth, cash flow growth and etc. but if it does not become converted to shareholder equity growth per share over time, the share price doe not hold up well from one economic cycle to another. The correlation of price performance to shareholder equity growth per share is a strong relationship.

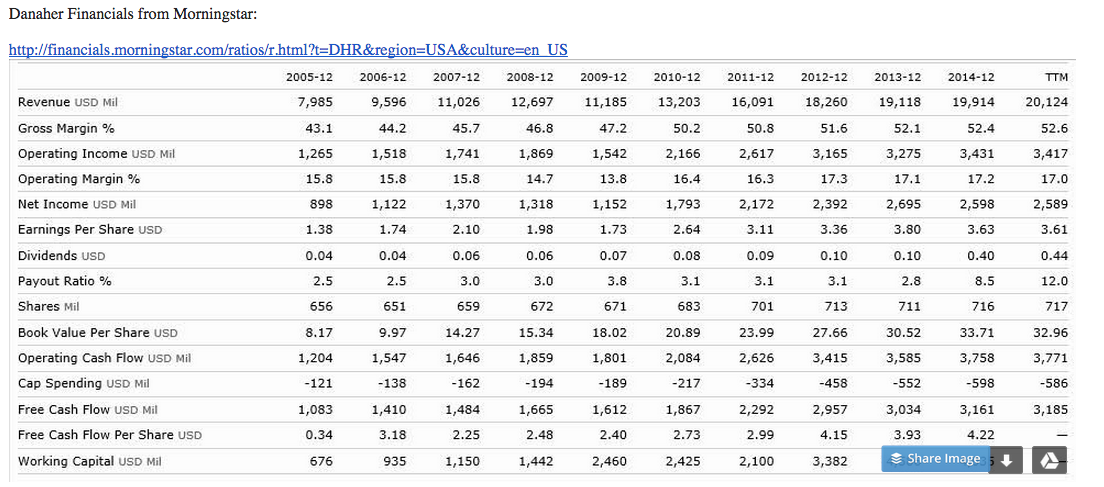

That Danaher’s management focuses on this parameter may come from the fact that the Steve and Mitch Rales have strong family roots in real estate. Danaher was a real estate company before it began to diversify into the industrial space. Real estate is an asset value business. The asset has a business use which generates returns and those returns must be in the context of current economic returns elsewhere. For one to be successful one must make sure that one’s valuation of one’s business assets, one’s Book Value, is honest and within the context of the fair market value of those assets. This is how real estate investors think. They are asset based investors-see Danaher’s Morningstar financial table below. Mark Papa of EOG is a good example of asset based thinking in the energy industry. He once told me he did not understand Wall Street’s thinking when it ignored shareholder equity as a valuation metric.

When CEO’s manage to consistently grow Book Value per Share(BV/Shr), investors get consistent performance over time. Danaher is only one example where BV/Shr growth has been consistent. Many of the current market favorites have little or non-existent growth in BV because they are spending as or even more rapidly than they are earning. We see revenue growth, we see cash flow growth, but no growth in shareholder equity to speak of. Companies which have had growth in shareholder equity have assets against which lending institutions will lend even during difficult times. Companies which have low shareholder equity during difficult times often find few are willing to lend to them to bridge these periods.

I like to see not only consistent growth in BV/Shr, but I like to see a Pr/BV at a level which makes economic sense(the lower the Pr/BV-the higher the return for investors all things being equal). Highly mentioned companies in the media sport 10-20x Revenue(Sales) and 10-50x BV/Shr. For some one looking for a return on assets as a business metric, these companies often show a relatively low growth rate of BV/Shr which makes any stock purchase at 10xBV a return dilution by a factor of 10. Not something I can recommend to my investors. Yet, there are many who rush in simply because prices are rising regardless.

If you think like a real estate investor, you will only think about buying a stock when everyone else is selling. Investing is decidedly not a team sport, but the realm of individual contrarians. You want the own the Danahers of the world when their shares represent good business returns.