The refrain seems to be that because we had set a record for consecutive 200k+ monthly jobs gains, anything less than this immediately means we are sliding into recession. It is almost as if we now think economic data does not ebb and flow and one or two month’s numbers are a “new trend” (and that trend immediately goes from record results to recession). Of course we ignore record auto sales, retail sales, strengthening construction etc etc and focus on the one number that isn’t where we want it to be.

The basic point is that we still added 142k jobs (1st read). We also should note that the last three years saw September’s number revised UP from between 18k to 27k jobs. Further, ~3MM more people are working today than they were at this time last year (and they are getting paid more) and there is one other labor market anomaly to think about, the changing US worker is increasingly not being counted in official labor statistics:

But that total is well shy of a projection made earlier this week in an MBO Partners independent labor report, which estimates the domestic economy holds 30.2 million independent workers who are at least 21 years old. The country’s independent workforce has ballooned 12 percent in the last five years alone, according to the report – which dwarf’s the overall labor market’s 2 percent growth over the same period.

“Over the past year, independent workers generated more than $1.15 trillion of revenue. That sum, equal to nearly 7 percent of U.S. GDP, was up 5.8 percent from 2014 and is 26 percent higher than the 2011 total,” the report said. “The independent workforce is growing at a rate that is more than four times greater [than] the growth rate of the overall workforce.”

The discrepancy in the two projections is partly because the Labor Department counts self-employed workers whose businesses are incorporated – or legally distinguished as free-standing corporate entities – as standard wage and salary workers. And full-time employees who do consulting or freelancing work on the side are often skipped over in the tallying of self-employed labor each month.

This means thousands of temporary employees and freelancers aren’t technically counted as self-employed in the Labor Department’s calculations. It also means the health of the country’s freelance economy can potentially be undervalued.

“Davidson” submits:

According to CNBC ‘Experts’ after this morning’s employment report, this week’s data indicate that the economy is in dire straits. Each ‘Expert’ on this morning’s panel tried to talk-over the others in being more pessimistic. If you heard the commentary, you would think our economy had had literally zero improvement since 2009 especially in in Personal Income growth. I am long beyond being shocked at the lack of basic analysis which has been prevalent in the financial industry, but the commentary this morning was particularly misinformed in my opinion.

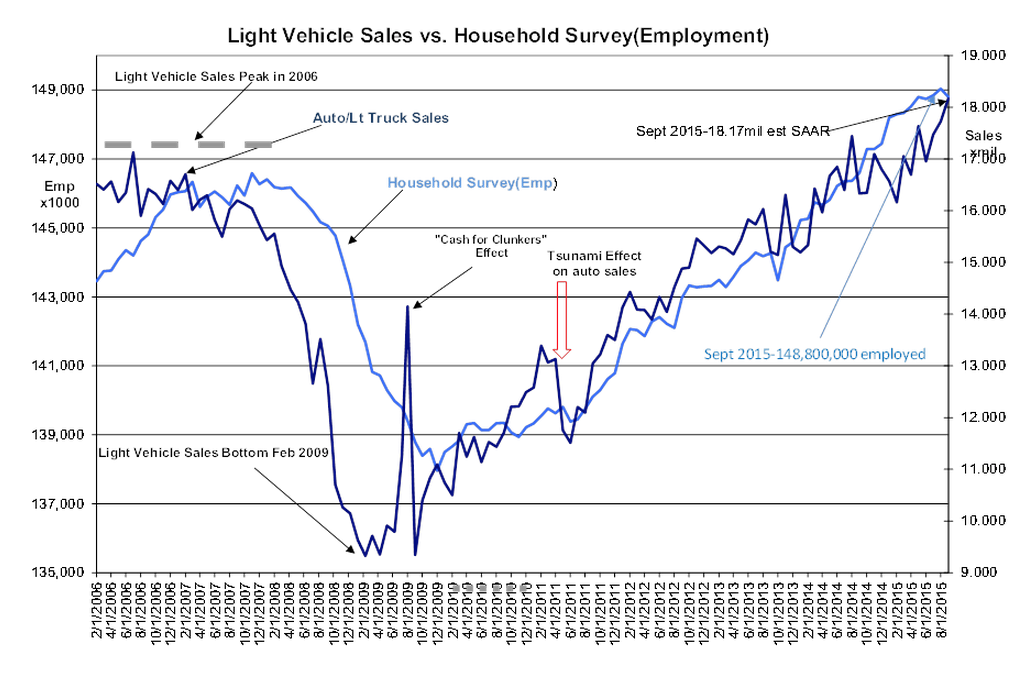

The Light Vehicle Sales vs. Household Survey chart shows where we have come since early 2009. The US economy has had a decent economic recovery since early 2009 as reflected in vehicle sales and employment levels. Employment levels are at record levels. The very reliable economic measures we have available, time tested and improved countless times, show we have been and remain in economic expansion since early 2009. This week’s data, even with a drop in Household Survey Employment of 236,000, show that economic trends within our statistical methodology continue higher.

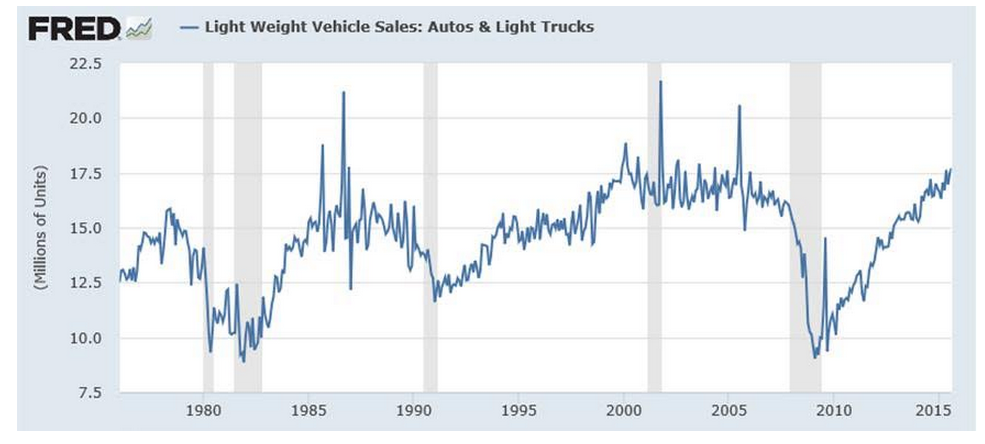

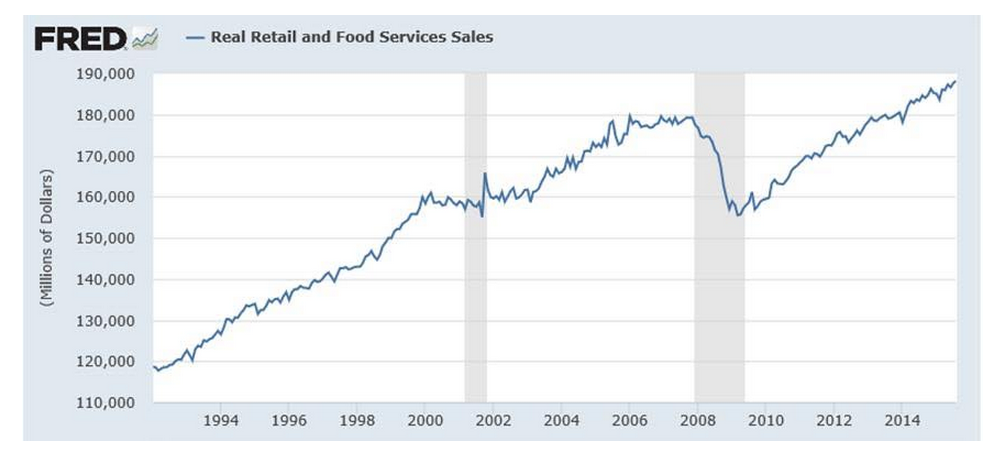

One comment made this morning on CNBC which was grossly misleading had to do with Personal Income growth which was discussed as non-existent. I call your attention to a series of economic charts below which come from the St. Louis Fed site concerning historical vehicle sales, personal income and retail sales. Let me walk you through each in turn.

1) The history of vehicle sales shows that current rate is very high and still trending higher. The historical record reveals that at some point the sales trend eventually levels off and continues at high levels for 3yrs-4yrs prior to the next recession. We have yet to reach a sustained sales level. Sales are still rising!

2) The history of personal income shows that contrary to consensus and contrary in particular to the pessimism carried in the media personal income is at historical highs and continues higher.

3) Retail and food service sales (of which vehicle sales are a part) are highly correlated to increases in personal income.

The often repeated statement that markets have only risen to current levels because the Fed has kept interest rates so low is without merit. Markets have risen since 2009 because there has been a real economic recovery with real increases in employment, personal income, retail sales, corporate profits and expansion in global commerce.

With pessimism having been ratcheted higher today, in my opinion investor response should be to buy LgCap Domestic and Intl equities as well as Natural Resource issues. Once this highly pessimistic psychology is turned by continuing economic expansion and the ‘Good News’ which eventually drives many a Momentum Investor, we could see a dramatic rise in the equity markets. History supports a positive turn in market psychology during economic expansions. Predicting when this turn will occur is not possible.

Buy stocks/Exit bonds!!!