“Davidson” submits:

The past 12mos has seen many a ‘high profile’ investor forecast that a recession is imminent. This is the consensus view. Some claim it is driven by economic weakness from one area or another. There are still claims that employment is weak when it is at record highs. Others claim that retail sales and personal income (wage growth) are nearly unchanged for more than a decade. Not so! They are much better. Then, there are those who claim that recoveries only last a certain number of years before they expire. Not so! Finally, there are some who claim no recovery has occurred and that the SP500 is only higher because interest rates are so low, i.e. high stock prices are only supported by the Federal Reserve keeping interest rates at historical lows. Definitely, not so! The range of commentary covers a broad spectrum, but remains pessimistic just the same. Lately the consensus is calling for the Fed to raise rates with the stated goal that higher rates stimulate economic activity. Every once in a while a Value Investor comments that stock prices are reasonable, economic expansion should continue and the Fed should leave rates alone. I agree with the Value Investors.

Recessions have an economic signal:

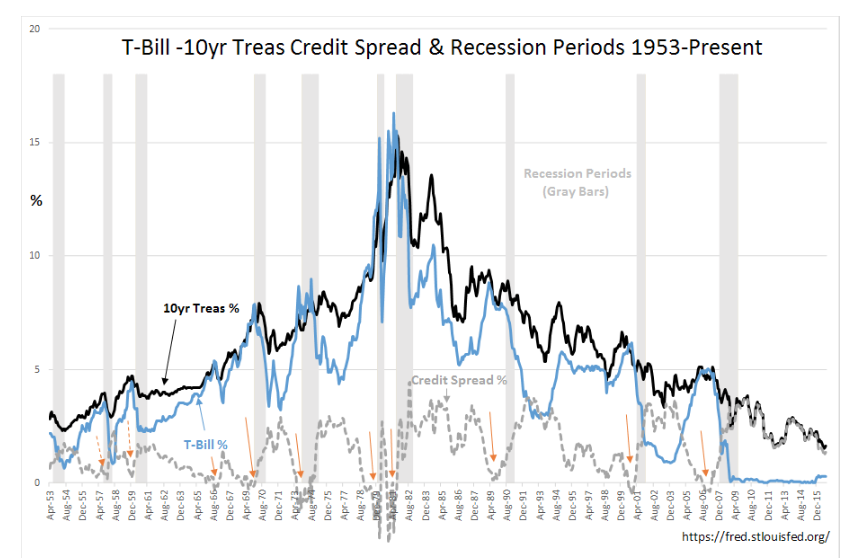

There is a strong correlation between recessions and the spread of 10yr Treas minus T-Bill rates. When this spread drops to zero, the yield curve becomes flat or even inverted. This pattern is observed in T-Bill -10yr Treas Credit Spread & Recession Periods 1953-Present. The 10yr Treasury Rate is shown by the BLACK LINE, the T-Bill rate is shown by the BLUE LINE and the difference in these rates is shown by the DASHED GRAY LINE. The RED ARROWS point at periods when the rate spread were 0.0% or less followed by a recession. TheDASHED RED ARROWS indicate periods when the rate spread did not quite reach 0.0% followed by recession. The correlation between at or near 0.0% rate spreads between T-Bills and the 10yr Treasury and the onset of recessions is high.

All modern economic activity has a lending cycle. The level of lending is dependent on the this rate spread. Banks are intermediaries, offering saver deposits pegged to T-Bills or 2yr Treas rates (depending on saver’s time commitment) and lending to businesses rates pegged to LIBOR and home buyers with mtgs pegged to the 10yr Treas with a 160bps premium. The rate spread is where banks make profits. Spreads must be wide enough to cover operating expenses and underwriting risks. When economic activity becomes robust, it draws in a high level of speculation. Optimism is contagious and spills into underwriting standards resulting in over-leveraging of bank assets with higher risk. As optimism percolates throughout the economy, T-Bill rates rise as investors, becoming overly optimistic, throw caution to the wind and sell T-Bills to seek higher returns. There is a period of unsustainable economic growth above historical levels. Lending becomes automatically choked-off when T-Bill rates rise enough to equal 10yr Treas rates creating a 0.0% interest spread between deposits and loans. Lending profits are offset by higher than expected charge-offs. Lending stalls sharply. Recessions follow! Since 1953, only 1966 stands out as only instance when the rate spread moving to 0.0% did not produce a recession.

Recessions, for the most part, in my opinion, are predictable. The rate spread between T-Bills and the 10yr Treasury is 1.20% today or 120bps(basis points). Based on history, lending continues, a relatively high level of pessimism continues and so does economic expansion. The rate spread is only one of several economic measures we have available that indicates economic expansion is likely to continue for several years.

The persistent belief that the Fed controls rates:

The real fly-in-the-ointment in historical and even today’s thinking is the consensus belief that the Fed controls rates. Here is a 2000 reference which reflects this long-held belief.

https://www.thestreet.com/story/1156889/1/how-does-the-fed-funds-rate-affect-treasury-bills.html

“…interest-rate moves — by increases or decreases in the fed funds rate by the Fed (and) affect Treasury bill yields…”

…and another…

http://www.palisadeshudson.com/2014/01/the-forgettable-crash-of-1966/

“That 1966 crash came after two decades of nearly uninterrupted economic growth and stock market gains following World War II. As Vietnam and Johnson’s Great Society social programs began to push up government spending, the Federal Reserve responded by tightening credit conditions early in 1966. After hitting new highs in January and March of that year, the Standard & Poor’s 500 index dropped about 22 percent over the next eight months. It then rallied to even higher heights by early 1968, as the spending-fueled economy drove corporate earnings upward. The 1966 market downturn did not trigger a recession and never became a factor in the 1966 or 1968 elections. It was soon forgotten.”

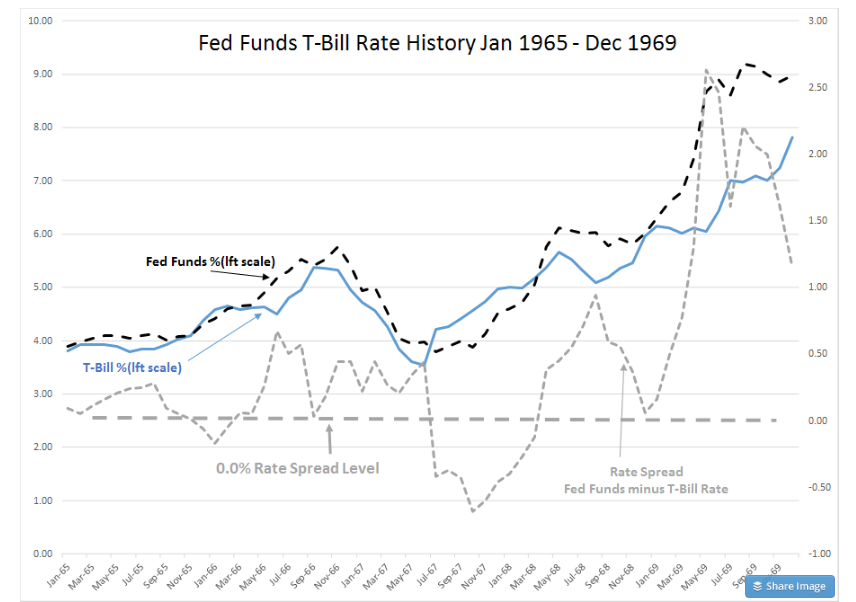

In looking at the details of 1966 rates, if one takes the time to plot T-Bill rates vs Fed Fund rates and plot the difference, it will be strikingly clear that the Fed has always acted after T-Bill rates rose or fell. The Fed has not controlled rates as most seem to believe. We have the data, it is only a matter of looking at it.

In looking at the details of 1966 rates, if one takes the time to plot T-Bill rates vs Fed Fund rates and plot the difference, it will be strikingly clear that the Fed has always acted after T-Bill rates rose or fell, Fed Funds T-Bill Rate History Jan 1965 – Dec 1969. How one sees this is in observing the directional spread of the rate difference in the calculation Fed Funds minus T-Bill rate. If the T-Bill % shifts and the Fed Funds % is adjusted afterwards the Rate Spread falls when T-Bill % rises and rises when the T-Bill % falls. That this occurred in 1966 shows that the Fed followed not led rate changes. The Fed has long had a history of following T-Bill rates. The Fed has not controlled rates as the consensus believes. We have the data, it is only a matter of looking at it. (The one instance in which the Fed actually exerted control was 1980-1981 when Chairman Volcker raised rates to a level corresponding to Knut Wicksell’s ‘Natural Rate’ after 1970’s period of high inflation and artificially low rates. Volcker’s actions stopped the rampant inflation behavior which had dominated the 1970s. Afterwards, Volcker and Greenspan adjusted Fed Funds in response to T-Bill rate changes)

With the lone example of Volcker’s 1980-1981 actions, Fed Funds have trailed T-Bill rate changes. Yet, consensus not only continues to believe that the Fed controls interest rates, but that higher rates will spur economic expansion. This confused perception puts the ‘cart-in-front-of-the-horse’. Higher rates are a result of improved economic activity. Higher rates do not stimulate economic expansion. Calling for higher rates is the same type of thinking which believed giving those who had poor credit histories would suddenly become financially prudent. My expectation is that should this Fed attempt to raise the Fed Funds rate further, either the T-Bill will not follow or markets will panic and drive the 10yr Treas rate lower with the effect of choking lending and slowing the economy. The Fed seeing a negative response will pause or even reverse a Fed Fund rise.

Economic expansion continues even with the consensus interpretation of conditions being misaligned with economic trends. In my opinion, economic expansion has several years to run. Housing, natural resource and infrastructure spending remain well below historical levels. Pessimism has kept future expectations subdued. Markets will not peak in my opinion till we have had a several years of optimism and economic excess.