“Davidson” submits:

Jim Cramer, a CNBC personality, created the acronym ‘FANG’ in 2013 to describe this cycle’s particular phenomena which has been a feature of every market cycle in history. FANG stands for Facebook, Apple, Netflix and Google. Every market cycle begins with Value Investor buying which creates a recession low. Value Investors create the major lows of every market cycle. Value Investors are investors who view investing through a long-term lens taking into consideration the long-term growth of the US economy in the context of the long-term global economic growth trends and then sort out individual companies they deem undervalued enough to produce future investment gains. As the economic cycle shows signs of improvement, Momentum Investors are drawn in by rising price trends. Momentum Investors believe all they need to know is in the price trend. Every market cycle is characterized by the perception and behavior of these two investor styles, Value and Momentum.

What is lost in the daily investment frenzy is that Value vs. Momentum use the same descriptive terms, i.e. “value”, “returns”, “growth”, but these terms mean entirely different things to each. So different is the meaning of “value” between Value and Momentum investors that neither understand the other’s perspective. A Value and Momentum Investor conversation is much like trying to mix oil and water.

What is seen in the media is roughly a 95% Momentum perspective. The reasons for this is markets have many twists and turns which feeds media reporting. Momentum Investors who base investment decisions on these twists and turns are always ready with commentary which satisfies the media need for new content. The media provides a constant stream of adjustments to stock and bond price targets to gain investor viewership. This is the basic ad revenue model. The constant focus on those investments which appear to be growing faster than others causes advisors to have an opinion on these issues as a means of gaining a media appearance. By having an opinion on a media favorite, advisory firms gain free advertising by proffering an opinion and the media receives free content. In this climate, certain issues become overly-reported and supported in every cycle. In the current cycle, Cramer coined the acronym ‘FANG’ to gain attention to his own commentary and drive view ship.

Every cycle has its issues which carry a ‘newness’ feature which make them appear different and highly desirable. Technology, Internet and Biotech issues have been those issues for recent cycles. Almost to an issue, they are more hope than substance. They carry investor expectations of gains well above average market returns and are always priced to extremes vs. market averages. Their Pr/Sales, Pr/Cash Flow, Price/Earnings are astronomical relative to market averages and justified by many advisors with commentary that ‘growth deserves high pricing’. In the midst of the market investment frenzy, the majority of investors come to believe that price-trends and positive surprises or market commentary justifies higher prices. Ignored are the true bottom-line growth metrics over time, i.e. the growth of Net Income and Book Value per Share, which represent actual long-term value for investors.

Every market cycle eventually incorporates the current group of ‘high growth’ issues into the indices against which quarter-to-quarter performance is judged. With dominance of indices by these over-priced and daily-hyped issues, investors tend to judge their own performance and economic activity by index price-trends. Every market cycle sucks investors into comparing their own returns with the price-trends of the most discussed issues. This is the situation today as underlined by this March 27, 2018 Bloomberg Technology Stocks Tumble headline. True growth actually lies elsewhere.

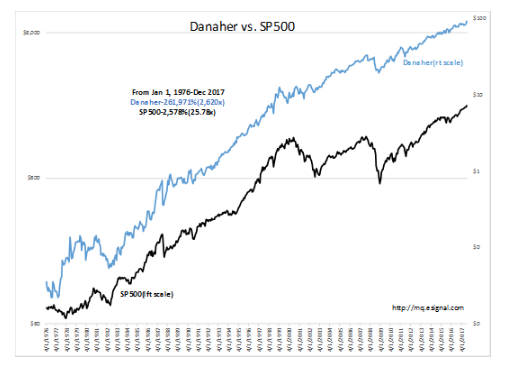

In the media’s desire to sell advertising by constantly refreshing viewership content, true growth issues are ignored. One of these is even today little known by most investors, Danaher(DHR). It is the DHRs of the world which are the true value creators of the US economy.

DHR has grown more than 100x than the SP500 in its history. It is a manufacturing company of thousands of industrial products which has made roughly 1,000 acquisitions since the 1970s and grown by making ordinary things profitably through the DBS(Danaher Business System). DHR is not the only company which has an exceptional long-term growth record that is much better than the SP500. Roughly 10% of companies have superior long-term performance relative to the SP500 and they rarely receive media attention. Companies like DHR, have consistent Net Income and Book Value per Share(Shareholder Equity per Share) growth and are responsible for the long-term performance of the indices. Because they have a slow news pace, they are nearly universally ignored by investors, Wall Street and the media.

The Investment Thesis:

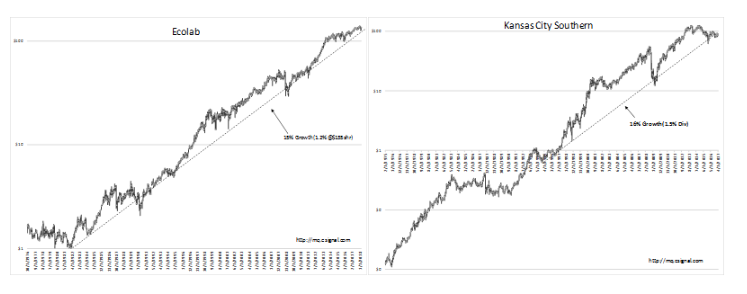

The secret to finding these types of companies is that it is not a secret at all. However, one does have to seek them out. One identifies them by seeking long-term price performance which is coupled to long-term underlying business financial performance. Market pricing always reflects cycles of market psychology which provides numerous opportunities to buy issues cheaply. Two companies which fit these criteria are Ecolab(ECL) and Kansas City Southern(KSU). The 1st produces hygiene products and the 2nd is a railroad. The common denominator is that both companies have exceptional managements.

The key to locating great investments is the identification of very good management teams. That is the secret to exceptional investment returns over time. In the Russell 3000, there are roughly 200 companies responsible for the long-term performance of this index. Owning these issues at the right price is how one out-performs any index.