“Davidson” submits:

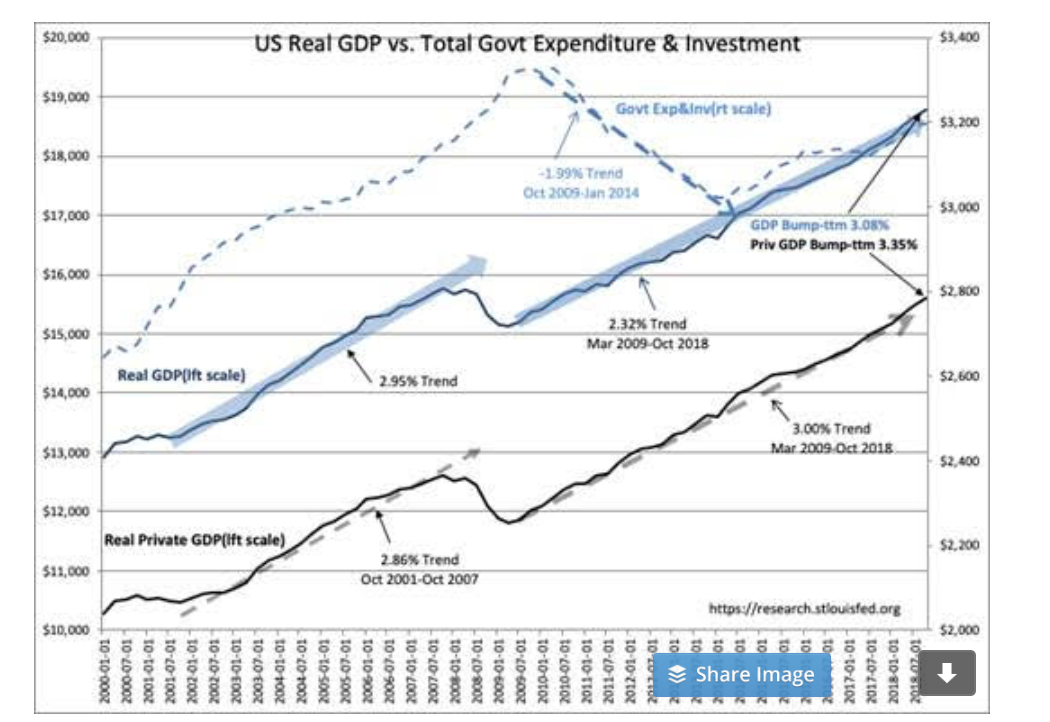

The Oct 2018 GDP reveals a nice bump above the longer term Trailing Twelve Month(ttm) trend. GDP includes Government Exp&Inv. The Private GDP excludes Government Exp&Inv to remove the influence from discretionary government spending which skews the true economic picture.

Real GDP: Trend Mar 2009-Oct 2018 2.32% and TTM 3.08%

Real Private GDP: Mar 2009-Oct 2018 3% and TTM 3.35%

The data represents the ttm as of Oct 2018. Earlier I noted that while there was a ‘bump’ in Government Exp&Inv that while we saw a rise in GDP, rise in Private GDP was not yet evident. Clearly, a rise in both measures has emerged. Two fiscal policies appear to be responsible, the sharp reduction in regulations implemented in 2017, -30% according to the Federal Register and tax reduction which began to be implemented in 2017. The Real Private GDP is the more important measure of underlying economic activity not skewed by government spending. Government spending has a decided impact on GDP. Just the same, Real Private GDP has risen more than 10% above trend which is a significant boost. Policy changes in place should help to maintain this pace going forward.

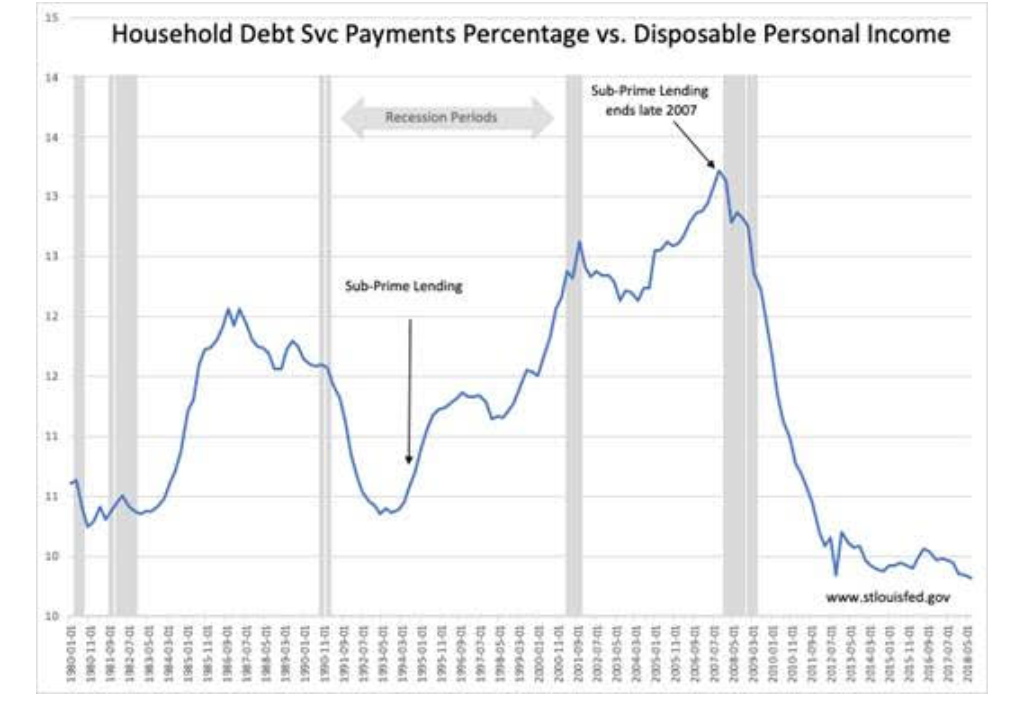

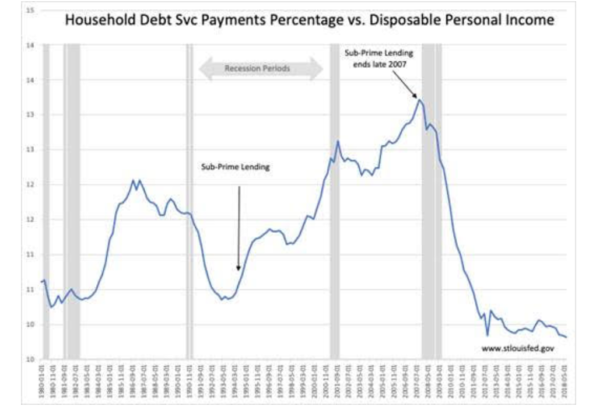

Even with this being 6mo old data, the trends look very healthy. The outliers for higher Real Private GDP lay in the potential for lowering global tariffs and easing of onerous lending regs which have resulted in a well recognized single-family housing shortage. Currently record low Household Debt service Payments to Disposable Personal Income indicates that there is very low household default risk the primary driver of past recessions.

All data is backwards looking, especially GDP data, but the acceleration seen with 2017 fiscal policy initiatives are likely to continue. If additional policy initiatives are successful, then additional rise in Real Private GDP towards 4% is quite possible.

All economic signs currently suggest significantly higher equity markets are likely the next few years.