“Davidson” submits:

Friday, Oct 28th, 2016 saw an FBI announcement and the market slip ~1% before recovering somewhat. There has been considerable discussion including whether this was a “Black Swan”. It was not!

“Black Swan” is a term coined by Momentum Investors for an unexpected event which causes a major market correction. Those who are Value Investors and follow economic data know that “Black Swans” only occur when economic activity has had a period of excess activity stimulated by excess lending. It should be obvious that we have not had a period of excess spending, home buying or a build-up of consumer debt. A period of excessive optimism has always been reflected in excessive stock prices.

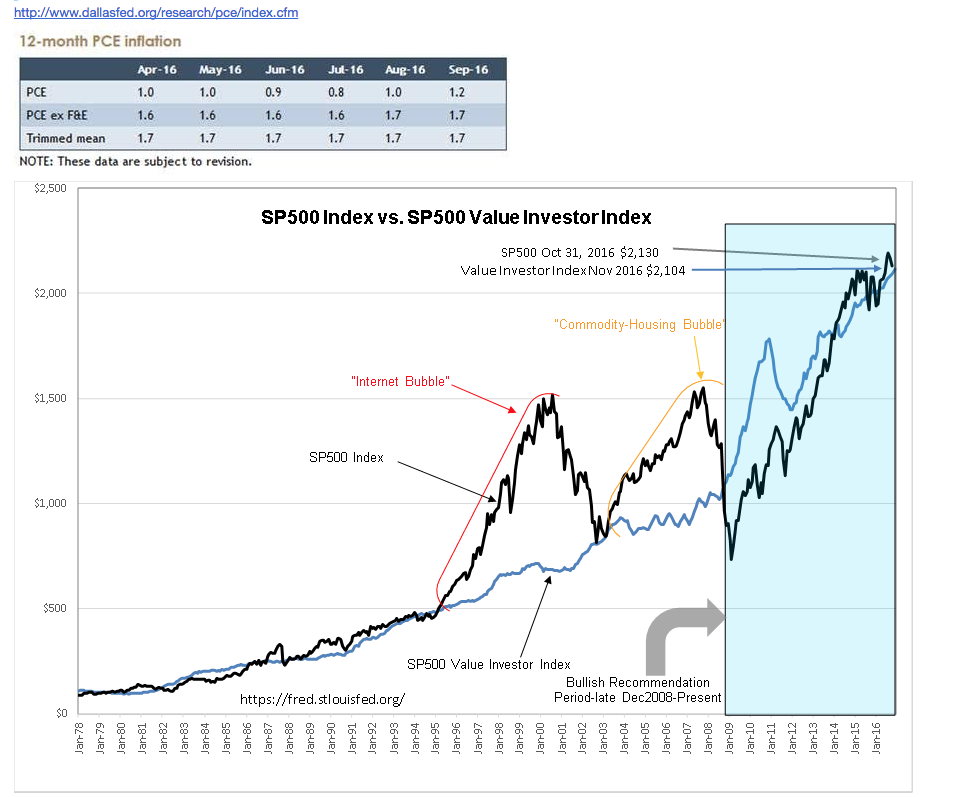

The SP500 Index vs. SP500 Value Investor Index shows the history of the SP500 Value Investor Index during 2000 and 2007 when markets had become over-priced relative to economic/business fundamentals. The sharp correction from these excess levels is where the term “Black Swan” is derived. The SP500 Value Investor Index reveals when the SP500is grossly over-priced. In 2000 and in 2007 the SP500 was ~100% over-priced. With the Dallas Fed 12mo Trimmed Mean PCE(inflation measure) reported this week at 1.7%, the SP500 Value Investor Index is $2,104 compared to the SP500 of $2,130. A $26 difference indicates that there is little excess pricing in the SP500.

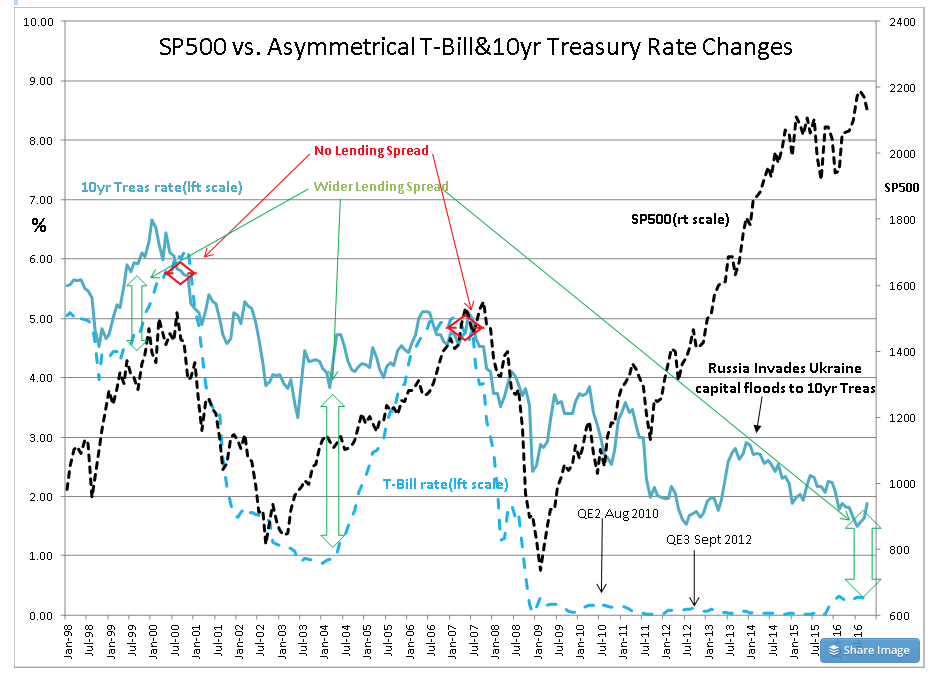

What does result in a major correction after a period of economic excess is a significant pull-back in lending. We can see this in SP500 vs. Asymmetrical T-Bill&10yr Treasury Rate Changes. It is when T-Bill rates rise to equal 10yr Treasury rates that lending to businesses and consumers slows significantly. In the past, this has only occurred when there has been a multi-year period of consumer and business spending resulting in above average economic growth. A period of positive economic changes has always resulted in market psychology which had been dominantly pessimistic changing to one of excessive optimism. The belief that returns can be gained without much risk leads investors to sell T-Bills to buy investments expecting higher returns. This forces T-Bill rates higher. During periods of optimism, consumers spend more than they have, businesses invest more than they should and banks lend more than is prudent. Once the rate spread between T-Bills and 10yr Treasuries shifts to 0.0%, lending profits are virtually eliminated and lending is sharply curbed.

The last 7yrs of economic activity leading to the current economic and market conditions are not conducive to a market correction. Recently, the 10yr Treasury rate has been rising (last week level 1.9%) while the T-Bill rate has slipped a little. The rate spread as shown in the chart has widened. This is a sign of economic strength. If this continues, we can expect an expansion of lending activity.

“Black Swans” have an economic basis which are easily monitored. Those who are not monitoring these conditions, often think that significant events can cause a “Black Swan”. “Black Swans” do not occur unless we have had a period of excess optimism. If the T-Bill-10yr Treasury rate spread continues to widen, we should see additional economic expansion, higher employment, higher corporate earnings and subsequently higher stock markets.

The equity markets have stalled for ~3yrs while general economic activity has continued in an uptrend. I expect higher equity prices the next several years.