“Davidson” submits:

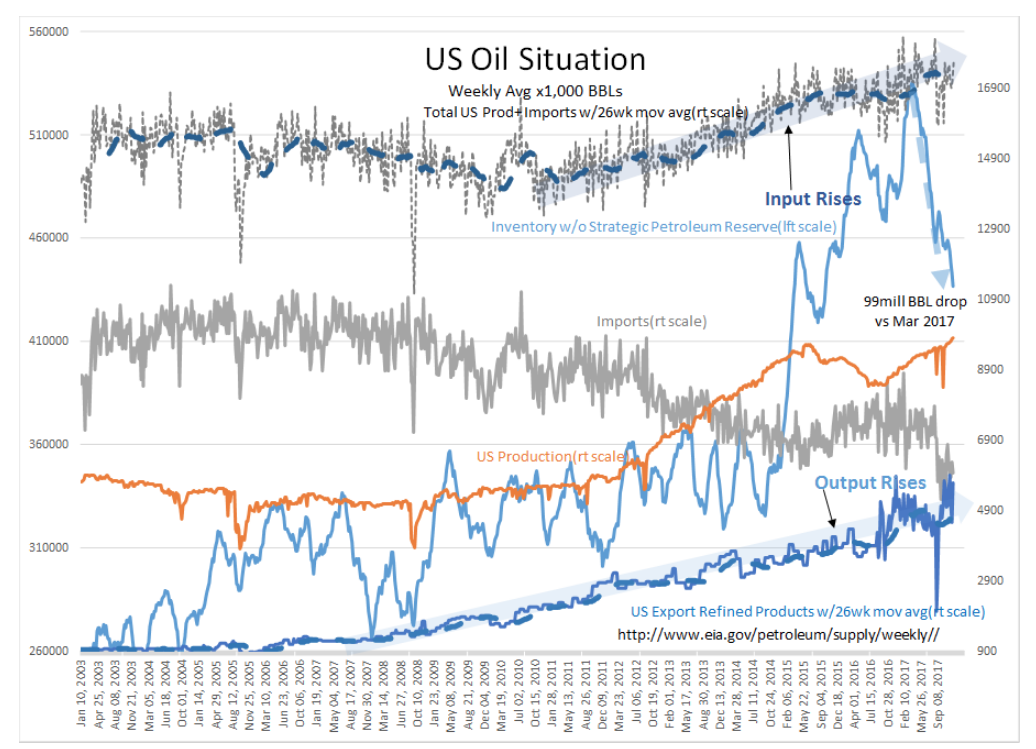

What is interesting is that the pessimists have ignored the drop in US crude inventories which are now ~100mil BBL from the March 2017 high. US Imports remain sluggish as we rely on domestic production to meet export of crude of 2mil BBL/Day and Refined Products of 5.5-6mil BBL/Day. US Oil Production continues to rise to new highs with a flat rig count as efficiencies let producers do more with each rig deployed.

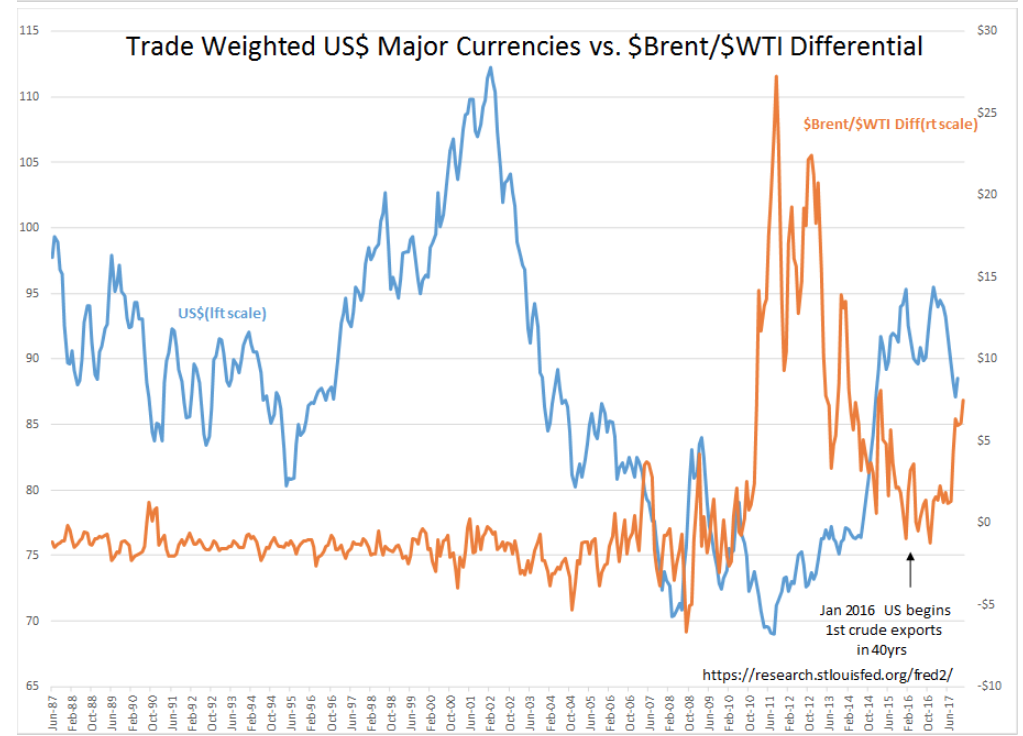

A new wrinkle is the sharp rise in $Brent vs. $WTI to $7.50/BBL. The last time we saw a sharp rise in this differential was 2010-2014, a period of $100BBL prices. This resulted in a of consumer/industrial efficiency and lower consumption. The high cost of $Brent vs. $WTI is again associated with lower imports and a huge draw-down in US Inventories. A draw-down never seen before!

I do not know how to interpret the US crude inventory drop, but it is interesting that commodity investors seem oblivious. Every 1mil BBL higher than expected inventory results in a drop in prices while lower than expected reports have been ignored. We still hear “Oil Glut” as the primary interpretation of any report.

With inventories falling and refining rising back to a rising trend now in the 18mil BBL/Day, rising Refined Product and crude exports, I expect at some point a sudden realization that the US inventories are short of required levels.

Price should rise in 2018